neurodoc

2025.03.01조회수 76회

neurodoc

구독자 69명구독중 35명

훌륭한 의사이면서

좋은 투자자가 되길 꿈꿉니다

*****경량화 해서 트레이딩뷰에서 돌리려고 숫자 줄여봤던 부분이 남아있어서 full LPPL로 코드 수정해서 올립니다.

글 내용도 수정됨*****

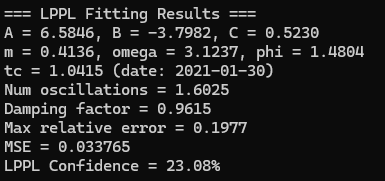

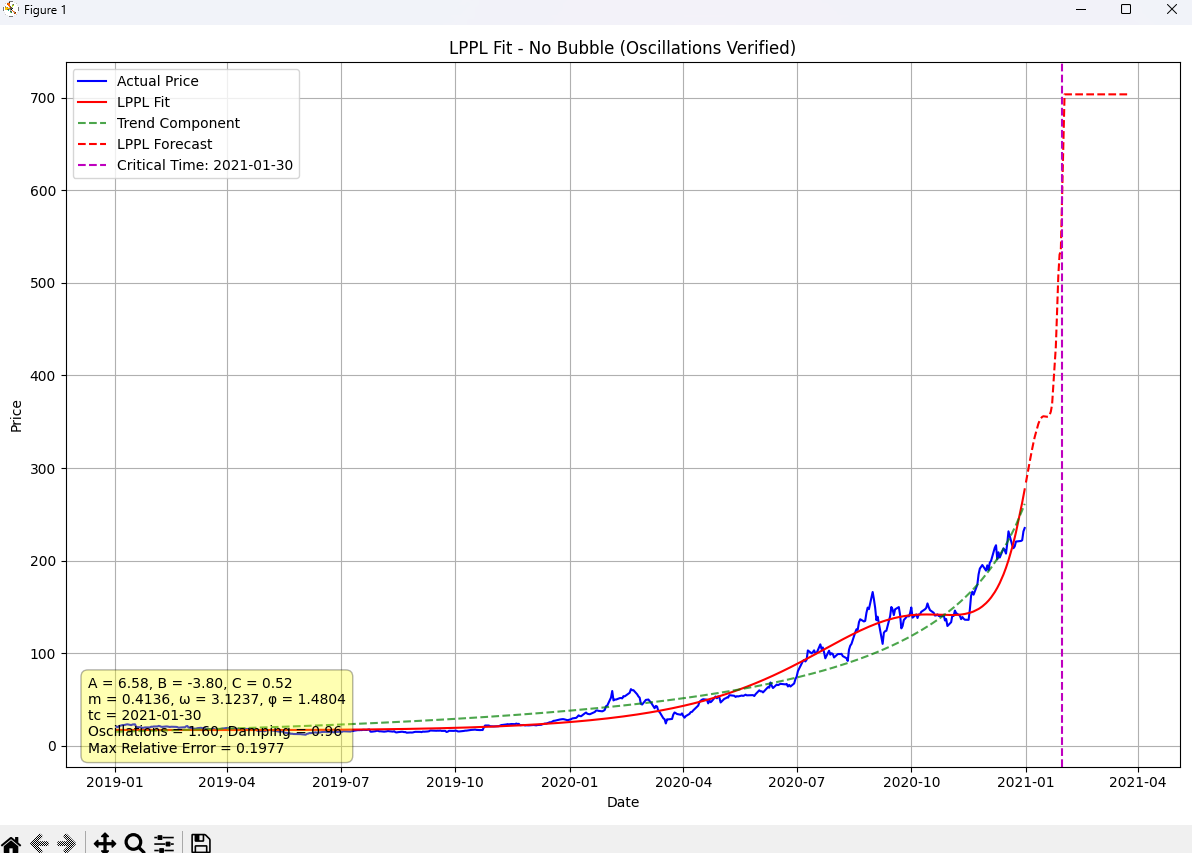

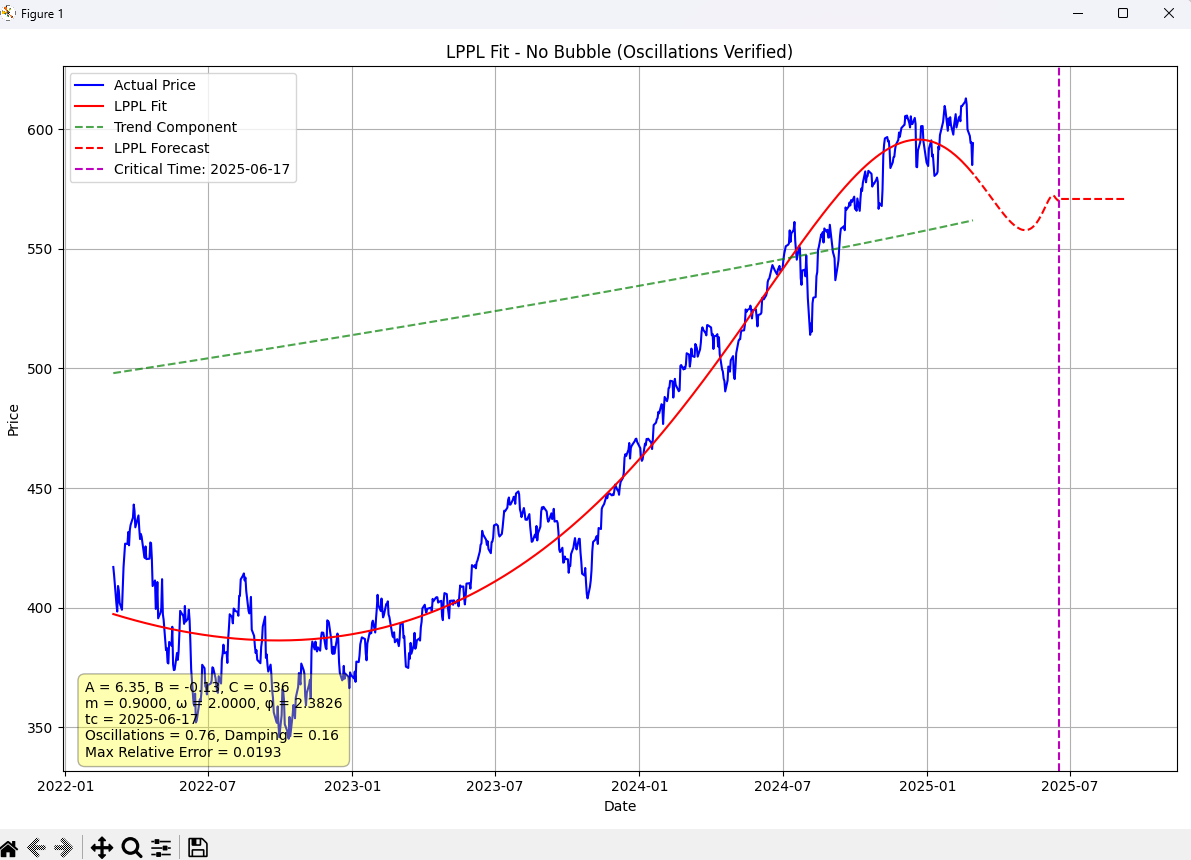

2019-01-01 ~ 2021-01-01 까지 TSLA 수정 종가를 바탕으로 한 분석 결과입니다.

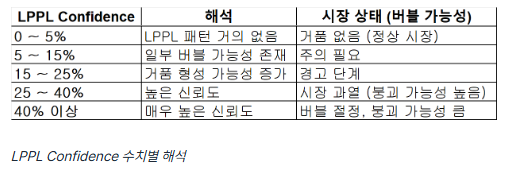

LPPL Confidence 23.08로 시장 과열에 가까운 경고단계

Critical time은 2021-01-30로 나왔습니다

이후 진짜로 그 쯤에서 버블이 꺼졌네요

자산군에 적용하는 것이 좋지만 만든김에 검증용으로 과거 테슬라 차트에 분석해봤습니다.

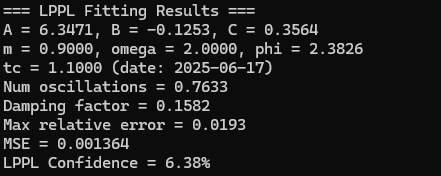

추가로 이미 퀀트팀에서 해주셨지만 SPY에 적용해볼까요?

오늘 날짜로 SPY는 LPPL confidence 6.38%로 주의필요 초기단계 쯤 되네요

앞으로 종종 모델 구현해서 공유해드리겠습니다.

아래는 만들어 본 코드입니다.(수정됨)

valley fellow 분들만 재미로 사용해보셨으면 합니다!

import numpy as np

import pandas as pd

import yfinance as yf

import matplotlib.pyplot as plt

from scipy.optimize import minimize

from scipy.linalg import lstsq

from datetime import datetime, timedelta

import warnings

import os

import time

import random

warnings.filterwarnings('ignore')

class LPPL:

def __init__(self, observations):

"""

Initialize the LPPL model with historical price observations.

Args:

observations (pd.DataFrame): DataFrame with a DatetimeIndex and 'Adj Close' column.

"""

self.observations = observations.sort_index()

self.t = self.get_days_since_start()

self.price = self.observations['Adj Close'].values

self.log_price = np.log(self.price)

# Scale time array to [0, 1] for optimization purposes

self.ts = self.t / self.t[-1]

# Parameter bounds based on typical LPPL references

self.bounds = {

'm': (0.1, 0.9),

'omega': (2, 25),

'phi': (0, 2 * np.pi)

# tc bounds will be set dynamically during fitting

}

# Genetic algorithm settings

self.population_size = 200

self.generations = 100

self.crossover_rate = 0.7

self.mutation_rate = 0.1

self.elitism_rate = 0.1

def get_days_since_start(self):

"""

Convert the DatetimeIndex into an array of days since the start date.

Returns:

np.ndarray: Array of days elapsed since the first date.

"""

start_date = self.observations.index[0]

return (self.observations.index - start_date).days.values

def lppl_matrix(self, t, tc, m, omega, phi):

"""

Construct the LPPL matrix for the given parameters.

Args:

t (np.ndarray): Scaled time array [0, 1].

tc (float): Critical time.

m (float): Bubble growth exponent (equivalent to beta in literature).

omega (float): Angular frequency of oscillations.

phi (float): Phase shift.

Returns:

np.ndarray: LPPL matrix of shape (n, 3).

"""

t = np.array(t)

dt = (tc - t).clip(0.00001) # Avoid numerical instability near zero

dt_pow_m = dt ** m

oscillatory = dt_pow_m * np.cos(omega * np.log(dt) - phi)

return np.vstack((np.ones_like(t), dt_pow_m, oscillatory)).T

def _func_(self, params, t, log_price):

"""

Objective function for non-linear parameter optimization.

Args:

params (np.ndarray): Parameter array [m, omega, phi, tc].

t (np.ndarray): Scaled time array.

log_price (np.ndarray): Log of the price series.

Returns:

float: Sum of squared errors.

"""

m, omega, phi, tc = params

try:

lppl_m = self.lppl_matrix(t, tc, m, omega, phi)

coefs = lstsq(lppl_m, log_price)[0]

return np.sum((log_price - lppl_m @ coefs) ** 2)

except (np.linalg.LinAlgError, ValueError):

return 1e10 # Large penalty on error

def simple_model_fit(self):

"""

Phase 1: Fit a simple model (C=0, beta=1) to obtain an initial seed for tc.

Returns:

tuple: (tc, A, B) as initial guesses.

"""

t_end = self.ts[-1]

def simple_obj(tc_val, t, log_price):

dt = tc_val - t

X = np.vstack((np.ones_like(t), dt)).T

try:

coefs = lstsq(X, log_price)[0]

return np.sum((log_price - X @ coefs) ** 2)

except np.linalg.LinAlgError:

return 1e10

# Set tc candidates from t_end + 0.01 to t_end + 0.1 (per strict criteria)

tc_candidates = np.linspace(t_end + 0.01, t_end + 0.1, 100)

errors = [simple_obj(tc_val, self.ts, self.log_price) for tc_val in tc_candidates]

best_tc = tc_candidates[np.argmin(errors)]

# Solve for A, B with best_tc

dt = best_tc - self.ts

X = np.vstack((np.ones_like(self.ts), dt)).T

try:

A, B = lstsq(X, self.log_price)[0]

except np.linalg.LinAlgError:

A = np.mean(self.log_price)

B = -0.01

return best_tc, float(A), float(B)

def initialize_population(self, tc_seed):

"""

Phase 2: Initialize the population for the genetic algorithm.

Modified: Set tc range to [t_end + 0.01, t_end + 0.1].

Args:

tc_seed (float): Initial tc seed from Phase 1.

Returns:

list: A list of tuples (params, fitness).

"""

population = []

t_end = self.ts[-1]

tc_low, tc_high = t_end + 0.01, t_end + 0.1

# First individual using tc_seed

initial_individual = np.array([

np.random.uniform(*self.bounds['m']),

np.random.uniform(*self.bounds['omega']),

np.random.uniform(*self.bounds['phi']),

tc_seed

])

fitness = self._func_(initial_individual, self.ts, self.log_price)

population.append((initial_individual, fitness))

# Remaining individuals

for _ in range(self.population_size - 1):

individual = np.array([

np.random.uniform(*self.bounds['m']),

np.random.uniform(*self.bounds['omega']),

np.random.uniform(*self.bounds['phi']),

np.random.uniform(tc_low, tc_high)

])

fitness = self._func_(individual, self.ts, self.log_price)

population.append((individual, fitness))

return population

def tournament_selection(self, population, tournament_size=3):

"""Tournament selection for the genetic algorithm."""

tournament = random.sample(population, min(tournament_size, len(population)))

return min(tournament, key=lambda x: x[1])

def crossover(self, parent1, parent2):

"""Crossover operation."""

alpha = np.random.random()

return alpha * parent1 + (1 - alpha) * parent2

def mutate(self, individual):

"""Mutation operation."""

m_strength = (self.bounds['m'][1] - self.bounds['m'][0]) * 0.1

omega_strength = (self.bounds['omega'][1] - self.bounds['omega'][0]) * 0.1

phi_strength = (self.bounds['phi'][1] - self.bounds['phi'][0]) * 0.1

tc_strength = 0.005 # Mutation strength for tc

result = individual.copy()

if np.random.random() < 0.3:

result[0] = np.clip(result[0] + np.random.normal(0, m_strength), *self.bounds['m'])

if np.random.random() < 0.3:

result[1] = np.clip(result[1] + np.random.normal(0, omega_strength), *self.bounds['omega'])

if np.random.random() < 0.3:

result[2] = np.clip(result[2] + np.random.normal(0, phi_strength), *self.bounds['phi'])

if np.random.random() < 0.3:

t_end = self.ts[-1]

tc_low, tc_high = t_end + 0.01, t_end + 0.1

result[3] = np.clip(result[3] + np.random.normal(0, tc_strength), tc_low, tc_high)

return result

def genetic_algorithm_fit(self, tc_seed):

"""

Phase 2-3: Optimize LPPL parameters using the genetic algorithm.

Args:

tc_seed (float): Initial tc seed from Phase 1.

Returns:

tuple: (best_params, best_fitness)

"""

population = self.initialize_population(tc_seed)

best_params, best_fitness = min(population, key=lambda x: x[1])

for generation in range(self.generations):

population.sort(key=lambda x: x[1])

elite_count = max(1, int(self.population_size * self.elitism_rate))

new_population = population[:elite_count].copy()

while len(new_population) < self.population_size:

if np.random.random() < self.crossover_rate:

parent1 = self.tournament_selection(population)[0]

parent2 = self.tournament_selection(population)[0]

child = self.crossover(parent1, parent2)

if np.random.random() < self.mutation_rate:

child = self.mutate(child)

fitness = self._func_(child, self.ts, self.log_price)

new_population.append((child, fitness))

else:

new_population.append(self.tournament_selection(population))

population = new_population[:self.population_size]

current_best, current_fitness = min(population, key=lambda x: x[1])

if current_fitness < best_fitness:

best_params, best_fitness = current_best, current_fitness

# Early stopping if no improvement after 10 generations

if generation > 10 and abs(current_fitness - best_fitness) < 1e-6:

break

return best_params, best_fitness

def multi_run_genetic_algorithm(self, tc_seed, runs=3):

"""

Run the genetic algorithm multiple times to find the best result.

Args:

tc_seed (float): Initial tc seed from Phase 1.

runs (int): Number of runs.

Returns:

tuple: (best_params, best_fitness)

"""

best_overall_params = None

best_overall_fitness = float('inf')

original_mutation_rate = self.mutation_rate

original_population_size = self.population_size

for run in range(runs):

print(f"Genetic Algorithm run {run+1}/{runs}...")

self.mutation_rate = original_mutation_rate + (run * 0.05)

self.population_size = original_population_size + (run * 50)

params, fitness = self.genetic_algorithm_fit(tc_seed)

if fitness < best_overall_fitness:

best_overall_fitness = fitness

best_overall_params = params

self.mutation_rate = original_mutation_rate

self.population_size = original_population_size

return best_overall_params, best_overall_fitness

def fine_tune_parameters(self, params):

"""

Phase 3: Fine-tune parameters using local optimization.

Modified: Set tc bounds to [t_last + 0.01, t_last + 0.1].

Args:

params (np.ndarray): Initial parameters [m, omega, phi, tc].

Returns:

np.ndarray: Refined parameters.

"""

tuned_params = params.copy()

param_bounds = [

self.bounds['m'],

self.bounds['omega'],

self.bounds['phi'],

(self.ts[-1] + 0.01, self.ts[-1] + 0.1)

]

for idx in range(4):

def objective(x):

params_copy = tuned_params.copy()

params_copy[idx] = x[0]

return self._func_(params_copy, self.ts, self.log_price)

result = minimize(objective, x0=[tuned_params[idx]],

...

코드 공유까지!! 감사합니다!!

경량화 해서 트레이딩뷰에서 돌리려고 숫자 줄여봤던 부분이 남아있어서 full LPPL로 코드 수정해서 올립니다. 이전에 가져가신 분들인 500이랑 20으로 서치하셔서 500 -> 750, 20->5로 바꾸시면 됩니다.

와우 감사합니다:)

경량화 해서 트레이딩뷰에서 돌리려고 숫자 줄여봤던 부분이 남아있어서 full LPPL로 코드 수정해서 올립니다. 이전에 가져가신 분들인 500이랑 20으로 서치하셔서 500 -> 750, 20->5로 바꾸시면 됩니다.

확인했습니다! 감사합니다:)

이런 건 파이썬 1년 열심히 하면 만들 수 있는 건가요? 작년에 책 한번 봤지만 전혀 감을 못잡고 있어요..

요즘은 ai를 잘 활용하시면 초보적인 지식만으로도 가능합니다

경량화 해서 트레이딩뷰에서 돌리려고 숫자 줄여봤던 부분이 남아있어서 full LPPL로 코드 수정해서 올립니다. 이전에 가져가신 분들인 500이랑 20으로 서치하셔서 500 -> 750, 20->5로 바꾸시면 됩니다.

나름 개발 업무를 10년째 하고 있지만 저보다도 훨씬 더 대단하신 것 같습니다! 부끄럽지만 LPPL이 뭔지 몰라서 지금 관련 논문과 블로그를 찾아가면서 공부하고 있습니다. 한가지 여쭤보고 싶은 부분이 있는데요, 우선 generic algorithm에 사용하신 param들은 혹시 어떻게 설정하신 건가요? 참고하신 paper가 있는지 궁금합니다

다른 글 보다 valley 월간 퀀트스터디부터 보시면 좋을 것 같습니다. 너무 정리를 잘해주셔서 이해가 쏙쏙 됩니다 Koistinen, J. (2020). “THE LOG-PERIODIC POWER LAW: Evidence from the Finnish Stock Market”. Master’s Thesis, Aalto University School of Business. vally 퀀트팀에서 올려주신 글 보고 이 페이퍼 위주로 참고했습니다

경량화 해서 트레이딩뷰에서 돌리려고 숫자 줄여봤던 부분이 남아있어서 full LPPL로 코드 수정해서 올립니다. 이전에 가져가신 분들인 500이랑 20으로 서치하셔서 500 -> 750, 20->5로 바꾸시면 됩니다.

valley 퀀트 스터디가 있군요! 이번에 3기로 참여해서 아직 모든 기능을 살펴보지 못했는데 바로 살펴보도록 하겠습니다. 감사합니다~

3기 동기들 다 같이 열심히 공부합시다 ㅎㅎ

경량화 해서 트레이딩뷰에서 돌리려고 숫자 줄여봤던 부분이 남아있어서 full LPPL로 코드 수정해서 올립니다. 이전에 가져가신 분들인 500이랑 20으로 서치하셔서 500 -> 750, 20->5로 바꾸시면 됩니다.

너무 감사합니다

감사합니다!!

와 이런거 너무 좋은데요. 구독누르고 갑니다!

덕분에 파이선, 비주얼스튜디오 더듬더듬 깔고 실행까지 AI 도움 얻어 실행해봤습니다~ 아웃풋이 너무 멋집니다~ 엑셀 해 찾기 함수로 도전했었는 데 영 안맞더군요 ㅠ ..... GLD, QQQ 돌렸는 데 LPPL Confidence가 0% 이 나왔습니다..참고하실 분들 참고요~ ^^

코딩에 대해서 아는게 거의 없는 사람이지만, 이렇게 공부하시면서 작성한 것을 보니 적어도 이게 뭔지 공부는 해봐야겠다는생각이 듭니다. 덕분에 공부해보게되어 정말 감사합니다. GPT 들을 이용해서 reverse engineering 해보려고 합니다. ^^ 좋은 공부거리 주셔서 감사합니다. 요 포스팅 제 글에 인용해도 될까요?? (허접한 글이 될 것으로 예상되어 정말 거절하셔도 무방합니다. ㅎㅎㅎ)

저도 만드는데 ai 툴 도움을 많이 받았습니다 얼마든지 인용하셔도 괜찮습니다 ㅎㅎ

감사합니다. ^^