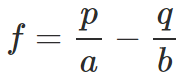

Kelly Criterion formula

f : Optimal Investment Size → 최적 betting 규모

p : Winning Probability → 승률(%)

q : Losing Probability (q = 1-p) → 실패율(%)

a : Loss of Negative Outcome → 실패시 (원금 대비) 손실율(%)

b : Gain of Positive Outcome → 승리시 (원금 대비) 수익률(%)

캘리 공식은

동일한 게임을 반복할 때

주어진 확률 분포에서

최적 투자금액(비율)을 계산하는 공식이다.

What is the Kelly criterion?

The Kelly criterion is a theoretical formula for obtaining the best return when repeatedly investing money. Sizing an investment according to the Kelly criterion can theoretically yield the best results.

Risks

The Kelly criterion requires clearly the ...

회원가입만 해도

이 글을 무료로 읽을 수 있어요.

이미 계정이 있으신가요?로그인하기

![[휘리릭 칼럼 읽기] Brain Rot !! 숏폼에 물들면 썩는 우리 뇌](https://post-image.valley.town/RTR1jYioX-BNmEUjPnzzx.png)

![[독서] The Primacy of Doubt #01](https://post-image.valley.town/IwFBndQXzd8f1V8vjDMm-.png)

![[투자공부] 지금 열심히 공부하면 나중엔 공부시간이 줄어들까?](https://post-image.valley.town/uFtuzLKl0dvUsD8Ssa0qX.png)

![[기후 지표와 천연가스 가격] ft. honestiores님 포스팅](https://post-image.valley.town/auUt9yz6m88ox3Q-8K2dg.png)