neurodoc

구독자 69명구독중 35명

훌륭한 의사이면서

좋은 투자자가 되길 꿈꿉니다

경량화 해서 트레이딩뷰에서 돌리려고 숫자 줄여봤던 부분이 남아있어서 full LPPL로 코드 수정해서 올립니다.

이전에 가져가신 분들인 500이랑 20으로 서치하셔서 500 -> 750, 20->5로 바꾸시면 됩니다.

이전 글에 수정해서 코드 올려뒀으니 이전 글 다시 확인하셔도 됩니다

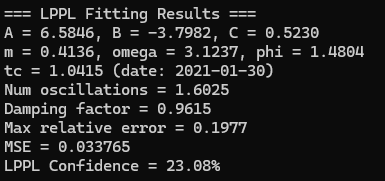

2025-03-03

LPPL 하락 분석 업데이트

import numpy as np

import pandas as pd

import yfinance as yf

import matplotlib.pyplot as plt

plt.rcParams['font.family'] ='Malgun Gothic'

plt.rcParams['axes.unicode_minus'] =False

from scipy.optimize import minimize

from scipy.linalg import lstsq

from datetime import datetime, timedelta

import warnings

import os

import time

import random

warnings.filterwarnings('ignore')

class LPPL:

def __init__(self, observations):

"""

LPPL 모델 초기화

observations: DatetimeIndex와 'Adj Close' 열을 포함한 DataFrame.

"""

self.observations = observations.sort_index()

self.t = self.get_days_since_start()

self.price = self.observations['Adj Close'].values

self.log_price = np.log(self.price)

self.ts = self.t / self.t[-1] # [0, 1] 범위로 스케일링

# 파라미터 bounds 설정

self.bounds = {

'm': (0.1, 0.9),

'omega': (2, 25),

'phi': (0, 2 * np.pi)

}

# 유전 알고리즘 설정

self.population_size = 200

self.generations = 100

self.crossover_rate = 0.7

self.mutation_rate = 0.1

self.elitism_rate = 0.1

def get_days_since_start(self):

"""

DatetimeIndex를 시작 날짜로부터 경과한 일수 배열로 변환.

"""

start_date = self.observations.index[0]

return (self.observations.index - start_date).days.values

def lppl_matrix(self, t, tc, m, omega, phi):

"""

주어진 파라미터로 LPPL 행렬 생성.

"""

t = np.array(t)

dt = (tc - t).clip(0.00001) # 0에 가까워지는 수치적 문제 방지

dt_pow_m = dt ** m

oscillatory = dt_pow_m * np.cos(omega * np.log(dt) - phi)

return np.vstack((np.ones_like(t), dt_pow_m, oscillatory)).T

def _func_(self, params, t, log_price):

"""

비선형 최적화를 위한 목적 함수.

"""

m, omega, phi, tc = params

try:

lppl_m = self.lppl_matrix(t, tc, m, omega, phi)

coefs = lstsq(lppl_m, log_price)[0]

return np.sum((log_price - lppl_m @ coefs) ** 2)

except (np.linalg.LinAlgError, ValueError):

return 1e10

def simple_model_fit(self):

"""

단순 모델 피팅(C=0, beta=1)으로 초기 tc 추정.

"""

t_end = self.ts[-1]

def simple_obj(tc_val, t, log_price):

dt = tc_val - t

X = np.vstack((np.ones_like(t), dt)).T

try:

coefs = lstsq(X, log_price)[0]

return np.sum((log_price - X @ coefs) ** 2)

except np.linalg.LinAlgError:

return 1e10

tc_candidates = np.linspace(t_end + 0.01, t_end + 0.1, 100)

errors = [simple_obj(tc_val, self.ts, self.log_price) for tc_val in tc_candidates]

best_tc = tc_candidates[np.argmin(errors)]

dt = best_tc - self.ts

X = np.vstack((np.ones_like(self.ts), dt)).T

try:

A, B = lstsq(X, self.log_price)[0]

except np.linalg.LinAlgError:

A = np.mean(self.log_price)

B = -0.01

return best_tc, float(A), float(B)

def initialize_population(self, tc_seed):

"""

유전 알고리즘 초기 개체군 생성.

"""

population = []

t_end = self.ts[-1]

tc_low, tc_high = t_end + 0.01, t_end + 0.1

initial_individual = np.array([

np.random.uniform(*self.bounds['m']),

np.random.uniform(*self.bounds['omega']),

np.random.uniform(*self.bounds['phi']),

tc_seed

])

fitness = self._func_(initial_individual, self.ts, self.log_price)

population.append((initial_individual, fitness))

for _ in range(self.population_size - 1):

individual = np.array([

np.random.uniform(*self.bounds['m']),

np.random.uniform(*self.bounds['omega']),

np.random.uniform(*self.bounds['phi']),

np.random.uniform(tc_low, tc_high)

])

fitness = self._func_(individual, self.ts, self.log_price)

population.append((individual, fitness))

return population

def tournament_selection(self, population, tournament_size=3):

tournament = random.sample(population, min(tournament_size, len(population)))

return min(tournament, key=lambda x: x[1])

def crossover(self, parent1, parent2):

alpha = np.random.random()

return alpha * parent1 + (1 - alpha) * parent2

def mutate(self, individual):

m_strength = (self.bounds['m'][1] - self.bounds['m'][0]) * 0.1

omega_strength = (self.bounds['omega'][1] - self.bounds['omega'][0]) * 0.1

phi_strength = (self.bounds['phi'][1] - self.bounds['phi'][0]) * 0.1

tc_strength = 0.005

result = individual.copy()

if np.random.random() < 0.3:

result[0] = np.clip(result[0] + np.random.normal(0, m_strength), *self.bounds['m'])

if np.random.random() < 0.3:

result[1] = np.clip(result[1] + np.random.normal(0, omega_strength), *self.bounds['omega'])

if np.random.random() < 0.3:

result[2] = np.clip(result[2] + np.random.normal(0, phi_strength), *self.bounds['phi'])

if np.random.random() < 0.3:

t_end = self.ts[-1]

tc_low, tc_high = t_end + 0.01, t_end + 0.1

result[3] = np.clip(result[3] + np.random.normal(0, tc_strength), tc_low, tc_high)

return result

def genetic_algorithm_fit(self, tc_seed):

"""

유전 알고리즘을 이용한 LPPL 파라미터 최적화.

"""

population = self.initialize_population(tc_seed)

best_params, best_fitness = min(population, key=lambda x: x[1])

for generation in range(self.generations):

population.sort(key=lambda x: x[1])

elite_count = max(1, int(self.population_size * self.elitism_rate))

new_population = population[:elite_count].copy()

while len(new_population) < self.population_size:

if np.random.random() < self.crossover_rate:

parent1 = self.tournament_selection(population)[0]

parent2 = self.tournament_selection(population)[0]

child = self.crossover(parent1, parent2)

if np.random.random() < self.mutation_rate:

child = self.mutate(child)

fitness = self._func_(child, self.ts, self.log_price)

new_population.append((child, fitness))

else:

new_population.append(self.tournament_selection(population))

population = new_population[:self.population_size]

current_best, current_fitness = min(population, key=lambda x: x[1])

if current_fitness < best_fitness:

best_params, best_fitness = current_best, current_fitness

# 개선이 없으면 조기 종료

if generation > 10 and abs(current_fitness - best_fitness) < 1e-6:

break

return best_params, best_fitness

def multi_run_genetic_algorithm(self, tc_seed, runs=3):

best_overall_params = None

best_overall_fitness = float('inf')

original_mutation_rate = self.mutation_rate

original_population_size = self.population_size

for run in range(runs):

print(f"유전 알고리즘 실행 {run+1}/{runs}...")

self.mutation_rate = original_mutation_rate + (run * 0.05)

self.population_size = original_population_size + (run * 50)

params, fitness = self.genetic_algorithm_fit(tc_seed)

if fitness < best_overall_fitness:

best_overall_fitness = fitness

best_overall_params = params

self.mutation_rate = original_mutation_rate

self.population_size = original_population_size

return best_overall_params, best_overall_fitness

def fine_tune_parameters(self, params):

"""

지역 최적화를 통한 파라미터 미세 조정.

"""

tuned_params = params.copy()

param_bounds = [

self.bounds['m'],

self.bounds['omega'],

self.bounds['phi'],

(self.ts[-1] + 0.01, self.ts[-1] + 0.1)

]

for idx in range(4):

def objective(x):

params_copy = tuned_params.copy()

params_copy[idx] = x[0]

return self._func_(params_copy, self.ts, self.log_price)

result = minimize(objective, x0=[tuned_params[idx]],

bounds=[param_bounds[idx]], method='L-BFGS-B')

if result.success:

tuned_params[idx] = result.x[0]

return tuned_params

def verify_oscillations(self, params):

"""

로그 주기적 진동의 유의미성을 확인.

"""

try:

num_oscillations = float(params['num_oscillations'])

damping_factor = float(params['damping_factor'])

if num_oscillations >= 2.0:

return True

if damping_factor >= 0.8:

return True

tc, m, omega, phi = params['tc'], params['m'], params['omega'], params['phi']

...