Divergence Emerges Between Human Traders and Computer-Driven Investors

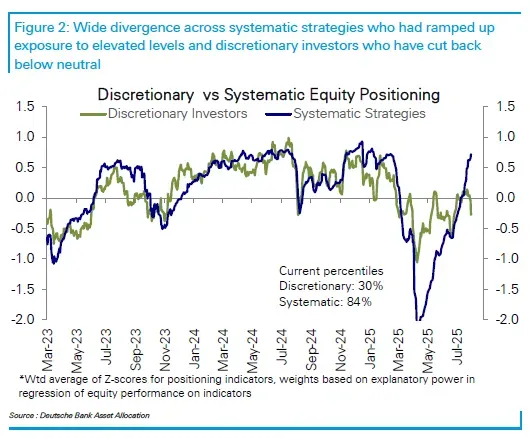

Computer-guided traders haven’t been this bullish on stocks compared to their human counterparts since early 2020, before the depths of the Covid pandemic, according to Parag Thatte, a strategist at Deutsche Bank AG.

The two groups look at different cues to form their opinions, so it’s not a shock that they see the market differently. While computer-driven fast-money quants use systematic strategies based on momentum and volatility signals, discretionary money managers are individuals looking at economic and earnings trends to guide their moves.

Still, this degree of disagreement is rare — and historically, it doesn’t last long, Thatte said.

“Discretionary investors are waiting for something to give, whether that’s slowing growth or a spike in inflation in the second half of the year from tariffs,” he said. “As the data trickles in, their concerns will either be proven right if the market sells off on growth fears, or the economy will remain resilient, in which case discretionary managers would likely begin to lift their stock exposure on economic optimism.”

도이치뱅크의 전략가 파라그 닷테에 따르면, 컴퓨터 기반의 트레이더들은 2020년 초 코로나19 팬데믹 심화 이전 이후로 현재와 같이 인간 트레이더들보다 주식에 대해 낙관적인 태도를 보인 적이 없다고 합니다.

두 그룹은 의견을 형성하기 위해 서로 다른 신호를 보기 때문에 시장을 다르게 보는 것이 놀라운 일은 아닙니다. 컴퓨터 기반의 '패스트 머니'를 운용하는 퀀트들은 모멘텀과 변동성 신호를 기반으로 하는 체계적인 전략을 사용하는 반면, 재량적 투자자들은 경제 및 실적 동향을 보고 투자 결정을 내리는 개인들입니다.

하지만 이 정도의 의견 불일치는 드물며, 역사적으로 오래 지속되지 않는다고 닷테는 말했습니다.

그는 “재량적 투자자들은 경기 둔화든, 하반기 관세로 인한 인플레이션 급등이든, 무언가 변화가 있기를 기다리고 있다”고 말했습니다. “데이터가 조금씩 나오면서 성장 둔화 우려로 인해 시장이 하락하면 그들의 우려가 옳았음이 증명될 것이고, 경제가 계속 회복력을 보이면 재량적 투자자들은 경제 낙관론에 따라 주식 비중을 늘리기 시작할 것입니다.”

“No one wants to buy pricier stocks already at records so some are praying for any selloff as an excuse to buy,” said Frank Monkam, head of macro trading at Buffalo Bayou Commodities.

버팔로 바이유 커머디티즈의 거시 트레이딩 책임자인 프랭크 몬캄은 "아무도 이미 기록적인 수준의 비싼 주식을 사려고 하지 않기 때문에, 일부 투자자들은 매수할 핑계를 만들기 위해 어떤 하락이라도 오기를 바라고 있습니다"라고 말했습니다.

Chasing momentum

Trend-following algorithmic funds, however, are chasing that momentum. They’ve been lured into a buying spree after cut-to-the-bone positioning in the spring cleared the path to return in recent months as the S&P 500 rallied almost 30% from its April low. Through the week ended Aug. 1, long equity positions for systematic strategies were the highest since January 2020, Deutsche Bank’s data show.

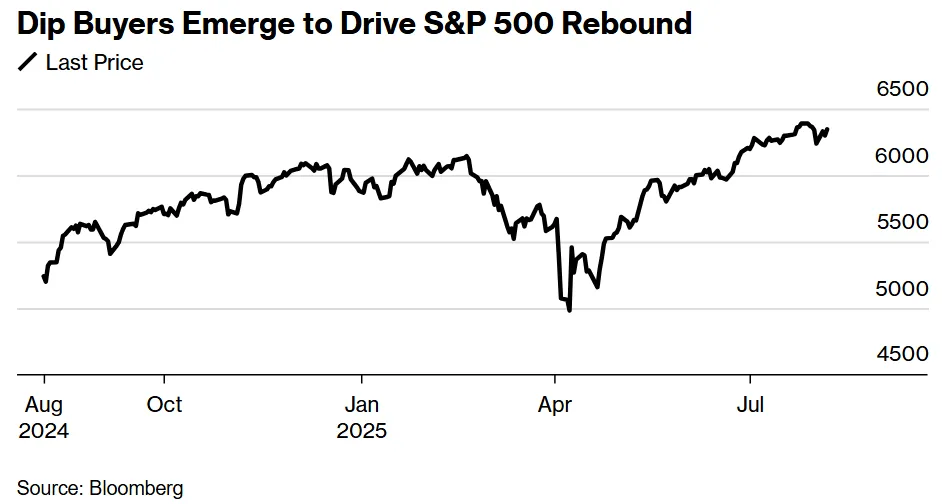

This divergence underpins the tug-of-war between technical and fundamental forces, with the S&P 500 stuck in a tight range after posting its longest streak of tranquility in two years in July.

The Cboe Volatility Index — or VIX — which measures implied volatility of the benchmark US equity futures via out-of-the-money options, closed at 15.15 on Friday, near the lowest level since February. The VVIX, which measures the volatility of volatility, dropped for the third time in four weeks.

“The rubber band can only stretch so far before it snaps,” said Colton Loder, managing principal of the alternative investment firm Cohalo. “So the potential for a mean-reversion selloff is higher when there’s systematic crowding, like now.”

반면, 추세 추종 알고리즘 펀드들은 이러한 모멘텀을 쫓고 있습니다. S&P 500 지수가 4월 저점 이후 거의 30% 반등하면서, 봄에 극도로 낮았던 포지션이 최근 몇 달간 다시 상승할 길을 열어주자, 이들은 매수세에 휩쓸렸습니다. 도이치뱅크의 데이터에 따르면, 8월 1일로 끝난 주간에 시스템적 전략을 위한 주식 롱 포지션은 2020년 1월 이후 최고치를 기록했습니다.

이러한 의견 불일치는 기술적 요인과 근본적 요인 사이의 힘겨루기를 보여주며, S&P 500은 7월에 2년 만에 가장 긴 안정세를 보인 후 좁은 범위에 갇혀 있습니다.

미국 주식 시장의 벤치마크 선물에 대한 내재 변동성을 측정하는 시카고옵션거래소 변동성 지수(VIX)는 금요일에 15.15로 마감하며 2월 이후 최저치에 근접했습니다. 변동성의 변동성을 측정하는 VVIX는 4주 만에 세 번째로 하락했습니다.

대체 투자 회사인 코할로의 매니징 프린시펄 콜턴 로더는 “고무줄은 끊어지기 전까지 한계까지 늘어날 수 있다”고 말했습니다. “따라서 지금처럼 시스템적 자금이 몰려들 때 평균 회귀로 인한 매도 가능성은 더 높습니다.”

CTA risk

Given how systematic funds operate, selling may start with commodity trading advisors, or CTAs, unwinding extreme positioning, Loder said. That would increase the risk of sharp reversals in the stock market, although there would need to be a substantial selloff for a spike in volatility to last, he added.

CTAs, who have been persistent stock buyers, are long $50 billion of US stocks, putting them in the 92nd percentile of historical exposure, according to Goldman Sachs Group Inc. However, the S&P 500 would need to breach 6,100, a decline of roughly 4.5% from where the index closed on Friday, for CTAs to begin dumping stocks, said Maxwell Grinacoff, head of equity derivatives research at UBS Group AG.

So the question is, with quant positioning this stretched to the bullish side and pressure building in the stock market due to extreme levels of uncertainty, can any rally from here really last?

로더는 체계적인 펀드가 운용되는 방식을 고려할 때, 매도는 상품 거래 자문가(CTA)들이 극단적인 포지션을 정리하는 것부터 시작될 수 있다고 말했습니다. 이로 인해 주식 시장에서 급격한 반전이 일어날 위험이 커질 수 있지만, 변동성 급등이 지속되려면 상당한 매도세가 있어야 한다고 그는 덧붙였습니다.

골드만삭스 그룹에 따르면, 꾸준히 주식 매수 포지션을 유지해 온 CTA들은 500억 달러 규모의 미국 주식에 대해 롱 포지션을 취하고 있으며, 이는 역사적 노출도의 92%에 해당합니다. 하지만 UBS 그룹의 주식 파생상품 리서치 책임자 맥스웰 그리나코프는 CTA들이 주식 매도를 시작하려면 S&P 500이 금요일 종가보다 약 4.5% 하락한 6,100선 아래로 떨어져야 한다고 말했습니다.

따라서 의문점은, 퀀트 포지션이 이렇게 강세로 치우쳐 있고 극도의 불확실성으로 인해 주식 시장에 압박이 커지는 상황에서, 과연 지금부터의 상승세가 지속될 수 있을까 하는 것입니다.

What’s more, any pullback from systematic selling would likely create an opportunity for discretionary asset managers who missed out on this year’s gains to re-enter the market as buyers, warding off a more severe plunge, according to Cohalo’s Loder.

“Whatever triggers the next drawdown is a mystery,” he said. “But when that eventually happens, asset-manager exposure and discretionary positioning is so light that it will add fuel to a ‘buy the dip’ mentality and prevent an even bigger selloff.”

더욱이, 코할로의 로더에 따르면, 시스템적 매도로 인한 어떤 하락이든 올해의 상승장을 놓친 재량적 자산 운용자들이 매수자로 다시 시장에 진입할 기회를 만들어 더 심각한 급락을 막을 가능성이 높다고 합니다.

그는 “다음 하락을 촉발할 요인이 무엇인지는 미스터리”라면서도, “하지만 그런 일이 결국 발생하면, 자산 운용사와 재량적 포지션이 너무 가벼워서 ‘하락 시 매수’ 심리에 불을 지피고 더 큰 매도세를 막을 것”이라고 말했습니다.

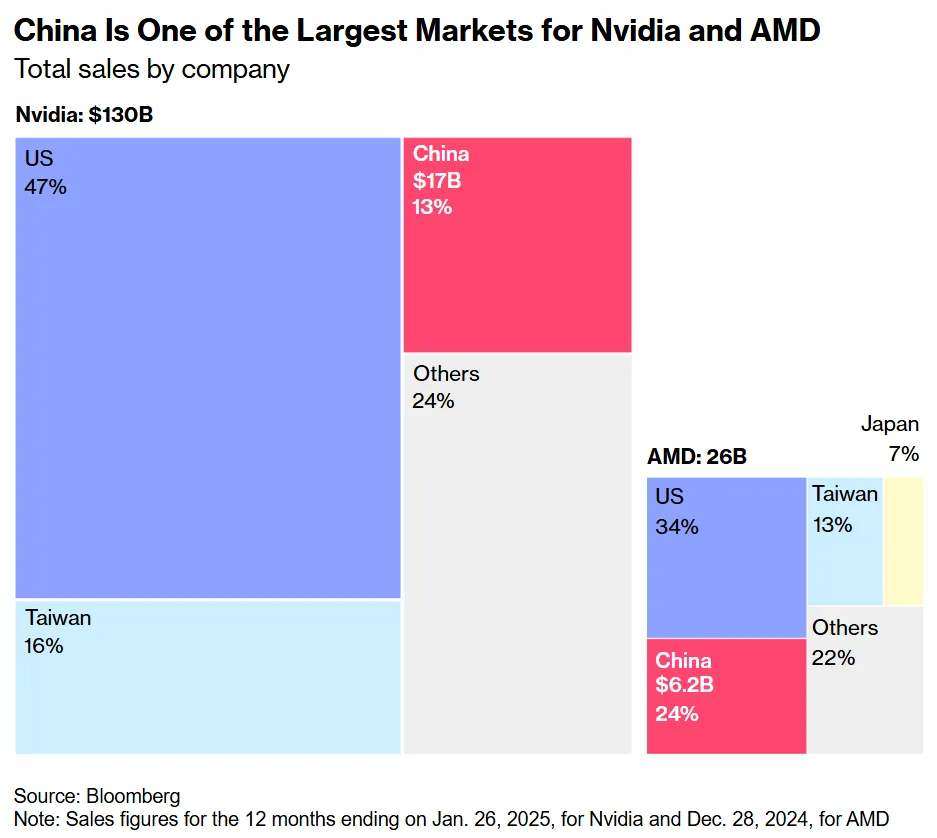

Nvidia, AMD to Pay US 15% of China AI Chip Sales in Trump Deal

Nvidia Corp. and Advanced Micro Devices Inc. agreed to pay 15% of their revenues from chip sales to China to the US government as part of a deal with the Trump administration to secure export licenses, the Financial Times reported Sunday.

엔비디아와 AMD가 중국에 대한 칩 판매 수익의 15%를 미국 정부에 지불하기로 트럼프 행정부와 합의하면서 수출 허가를 확보했다고 일요일 파이낸셜 타임스가 보도했습니다.

이번 정부는 말도 안될정도로 유연한 것 같은데

진짜 상상을 초월하네

Nvidia told the Financial Times that it follows US export rules, while AMD didn’t respond to the paper’s request for comment.

Separately, Intel Chief Executive Officer Lip-Bu Tan is expected to visit the White House on Monday after Trump called for his dismissal last week over his ties to Chinese businesses, the Wall Street Journal reported Sunday.

Nvidia는 파이낸셜 타임즈에 미국 수출 규정을 준수하고 있다고 말했으며, AMD는 논평 요청에 응답하지 않았습니다.

한편, 월스트리트 저널은 일요일에 트럼프가 지난주 중국 기업과의 유착 관계를 이유로 해고를 요구한 후 인텔의 최고 경영자 립-부 탄이 월요일에 백악관을 방문할 예정이라고 보도했습니다.

Hedge Fund Schonfeld’s Millennial Boss Drags It Back From the Brink

In an industry still ruled over by men of advanced middle age, and often much older, Ryan Tolkin’s relative youth has always stood out.

But when the 38-year-old boss of Schonfeld Strategic Advisors took to the stage at the New York hedge fund’s investor day in May, his words could have come from the mouth of any of his more seasoned rivals. “You’re never as good as your best day, and never as bad as your worst,” he told the audience.

Tolkin was 27 when he became chief investment officer for Steven Schonfeld’s then family office; 29 when he persuaded his dad’s childhood friend to take in outside money; and 34 when he was promoted to run the show. As he stood in front of a packed room of 100 or so investors and others, he had something new to offer: The bruises that came from surviving the biggest test of his leadership career — and of Schonfeld’s near four-decade existence.

Running a multistrategy hedge fund, the industry leviathans who stake teams running lots of different trades, is a ferociously cutthroat business at the best of times. One rough patch can turn into a death spiral if you haven’t structured the firm just right. And the past 36 months have been relentless for Tolkin.

A sudden burst of poor returns led some clients to withdraw money. The firm turned to larger rival Millennium Management to discuss a deal, making investors even more panicked. It had to pull together $3 billion of emergency cash in case things got worse. About 150 staff were fired.

That Schonfeld ended up nixing the Millennium deal and has left that rescue money untouched shows its staying power. Its rebound sets it apart from peers who’ve fallen by the wayside. But the saga also reveals a few inescapable truths in this industry: Spending generously on your own growth can fast become a noose around your neck if traders stop delivering; it’s dangerous making it too easy for clients to pull their capital; and when a hedge fund hits trouble, ruthlessness is always a major part of the cure.

While Tolkin has righted the ship, delivering record gains last year and getting client assets back up to $14 billion — after falling to $10 billion at the start of 2024 — he’s had to loosen his tight grip on the firm in the process.

Vital decisions are now being taken by beefed up executive and investment committees, people with knowledge of the situation say. Schonfeld himself opposed the Millennium option when the deal started to feel like a takeover, according to someone who knows him, putting in more of his own cash and letting his CEO sort out the cost base.

Tolkin had to cut 15% of staff, including about a dozen portfolio managers, shock therapy for an outfit that likes to shun this market’s brutal sackings. Breakneck expansion where headcount rose 20 times in eight years has been checked.

A longtime investor in Schonfeld funds, who asked to stay anonymous discussing sensitive commercial matters, points to its rapid growth and rising costs as the root cause of the troubles that weighed down its returns. The crisis that followed forced a necessary reset, he says, stripping things back to a more sustainable scale.

여전히 중년, 아니 훨씬 더 나이가 많은 남성들이 지배하는 업계에서 라이언 톨킨의 젊음은 항상 눈에 띄었습니다.

그러나 5월 뉴욕 헤지펀드 쇤펠트 스트래티직 어드바이저스의 투자자 행사에서 38세의 이 대표가 연단에 섰을 때, 그의 말은 그 어떤 노련한 경쟁자의 입에서 나온 말과 다름없었습니다. 그는 청중에게 "최고의 날이라고 해서 항상 좋은 것도 아니고, 최악의 날이라고 해서 항상 나쁜 것도 아니다"라고 말했습니다.

톨킨은 27세에 스티븐 쇤펠트의 당시 패밀리 오피스의 최고 투자 책임자가 되었고, 29세에 아버지의 어린 시절 친구를 설득하여 외부 자금을 유치했으며, 34세에 회사를 운영하게 되었습니다. 100여 명의 투자자와 관계자들로 가득 찬 방에서 그는 새로운 것을 보여줄 수 있었습니다. 바로 그의 리더십 경력과 쇤펠트의 40년 가까운 역사에서 가장 큰 시험을 이겨내고 얻은 훈장이었습니다.

다양한 트레이딩 팀을 운영하는 업계의 거물급 멀티스트래티지 헤지펀드를 운영하는 것은 최고의 시기에도 맹렬한 경쟁이 벌어지는 사업입니다. 한 번의 부진은 회사를 제대로 구조화하지 않으면 파멸의 소용돌이로 변할 수 있습니다. 그리고 지난 36개월은 톨킨에게 가혹한 시간이었습니다.

갑작스러운 수익률 부진으로 일부 고객들이 자금을 회수했습니다. 회사는 더 큰 경쟁사인 밀레니엄 매니지먼트와 협상을 논의했고, 이로 인해 투자자들은 더욱 공황 상태에 빠졌습니다. 상황이 악화될 경우에 대비해 30억 달러의 비상 자금을 마련해야 했습니다. 약 150명의 직원이 해고되었습니다.

결과적으로 쇤펠트는 밀레니엄과의 계약을 취소하고 비상 자금에 손대지 않았는데, 이는 회사의 저력을 보여줍니다. 쇠퇴의 길을 걸은 동료들과 달리 쇤펠트는 다시 회복했습니다. 그러나 이 이야기는 또한 업계의 몇 가지 피할 수 없는 진실을 보여줍니다. 즉, 성장을 위해 아낌없이 투자하는 것은 트레이더들의 성과가 부진할 때 목을 조르는 올가미가 될 수 있다는 것, 고객들이 자본을 너무 쉽게 인출하게 만드는 것은 위험하다는 것, 그리고 헤지펀드가 어려움에 처했을 때 무자비함이 항상 주요 해결책이라는 것입니다.

톨킨은 작년에 기록적인 수익을 달성하고 2024년 초 100억 달러까지 떨어졌던 고객 자산을 다시 140억 달러로 끌어올리며 회사를 정상 궤도에 올려놓았지만, 그 과정에서 회사에 대한 그의 굳건한 통제를 어느 정도 풀어야 했습니다.

상황에 정통한 사람들에 따르면, 이제 중요한 결정은 강화된 이사회와 투자 위원회에서 내려지고 있다고 합니다. 그를 아는 한 관계자에 따르면, 쇤펠트 본인은 밀레니엄과의 거래가 인수처럼 느껴지자 반대했고, 자신의 현금을 더 투입하여 CEO가 비용 구조를 정리하도록 했습니다.

톨킨은 150명 정도의 직원을 감축해야 했으며, 여기에는 약 12명의 포트폴리오 매니저가 포함되었습니다. 이는 잔인한 해고를 꺼리는 회사에게는 충격 요법이었습니다. 8년 만에 직원이 20배나 늘어났던 급격한...