20250826 News

Trump Says South Korea’s Lee Will Stick to Trade, Spending Deal

https://www.bloomberg.com/news/articles/2025-08-25/trump-blasts-south-korean-instability-ahead-of-president-s-visit

President Donald Trump refused to change the terms of South Korea’s tariff agreement, despite a lobbying effort from President Lee Jae Myung during their first in-person meeting.

Trump and Lee on Monday expressed optimism for close cooperation on North Korea, collective security and shipbuilding, yet the deal setting a 15% tariff on South Korean goods will remain unchanged, according to the US president.

도널드 트럼프 대통령은 이재명 대통령이 첫 대면 회담에서 로비 활동을 벌였음에도 불구하고 한국의 관세 협정 조건을 변경하는 것을 거부했습니다.

트럼프와 이 대통령은 월요일 북한, 집단 안보, 조선업에 대한 긴밀한 협력에 대해 낙관적인 태도를 보였지만, 미국 대통령에 따르면 한국 상품에 대한 15% 관세율을 정한 협정은 변함없이 유지될 것입니다.

The South Korean leader launched a charm offensive on Trump, praising stock-market gains, the gold finishes he added to the Oval Office and his peacekeeping efforts, and asked him to focus on ending tensions on the Korean peninsula. Lee even suggested that Trump could construct an eponymous tower in North Korea if peace is made.

이재명 대통령은 주가 상승, 그가 백악관 집무실에 추가한 금색 마감재, 평화 유지 노력을 칭찬하고 한반도 긴장 종식에 집중해달라고 요청하며 트럼프 대통령에게 매력 공세를 펼쳤습니다. 이 대통령은 심지어 평화가 이뤄진다면 트럼프가 북한에 자신의 이름을 딴 트럼프 타워를 건설할 수 있다고 제안하기도 했습니다.

Trump also congratulated Lee on his election and said “we’re with you 100%,” despite comments earlier Monday that questioned political stability in South Korea and further exacerbated tensions with the decades-old ally.

Both leaders nodded to a burgeoning shipbuilding agreement, with Trump pledging to purchase ships from South Korea and Lee acknowledging Trump’s desire to have Korean shipbuilding in the US employing American workers. Lee’s government is expected to unveil about $150 billion in US investment plans from private companies.

트럼프 대통령은 또한 이재명 대통령의 당선을 축하하며 "우리는 100% 당신 편"이라고 말했습니다. 이는 월요일 오전에 한국의 정치적 안정성에 의문을 제기하고 수십 년 된 동맹국과의 긴장을 더욱 악화시켰던 발언과는 상반되는 것입니다.

양 정상은 트럼프 대통령이 한국으로부터 선박을 구매하겠다고 약속하고 이 대통령이 미국 근로자를 고용하여 한국 조선업을 미국에서 하고자 하는 트럼프 대통령의 열망을 인정하면서, 번창하는 조선 협정에 고개를 끄덕였습니다. 이 대통령의 정부는 민간 기업으로부터 약 1,500억 달러에 달하는 미국 투자 계획을 발표할 것으로 예상됩니다.

The two sides reached a last-minute trade deal at the end of July that capped tariffs on US imports from South Korea, allowing Seoul to avoid the 25% rate that Trump had threatened to impose. But Trump administration officials had since signaled dissatisfaction over the terms and have been eager to pin down South Korea on the specifics of the $350 billion it pledged to invest in the US as part of the deal.

Monday’s meeting was also expected to touch on other thorny issues, including reaching an agreement on defense cooperation, which Seoul initially tried to make part of the tariff deal.

Trump earlier on Monday blasted South Korea for political instability on social media and elaborated on those comments during a signing of executive orders that stretched more than an hour, keeping Lee waiting past the leaders’ scheduled meeting time.

Trump mused on Truth Social that it seemed “like a Purge or Revolution” in South Korea, and later told reporters in the Oval Office that he’d heard “there were raids on churches over the last few days, very vicious raids on churches by the new government in South Korea, that they even went into our military base and got information.”

양측은 7월 말에 막판 무역 협정을 체결하여 한국산 미국 수입품에 대한 관세 상한선을 설정함으로써 한국이 트럼프 대통령이 부과하겠다고 위협했던 25% 관세율을 피할 수 있었습니다. 그러나 트럼프 행정부 관리들은 그 이후로 조건에 대한 불만을 표명했으며, 한국이 협정의 일환으로 미국에 투자하기로 약속한 3,500억 달러의 구체적인 내용을 확정 짓는 데 열심이었습니다.

월요일 회담에서는 한국이 처음에는 관세 협정의 일부로 만들려고 했던 국방 협력에 대한 합의 도출을 포함한 다른 민감한 문제들도 다뤄질 것으로 예상되었습니다.

트럼프 대통령은 월요일 오전에 소셜 미디어에서 한국의 정치적 불안정성을 맹비난했으며, 한 시간이 넘게 이어진 행정명령 서명식에서 이 발언을 자세히 설명하여 예정된 정상 회담 시간을 지나 이 대통령이 기다리게 만들었습니다.

트럼프 대통령은 소셜 미디어인 트루스 소셜에서 한국이 "숙청이나 혁명"처럼 보인다고 생각했으며, 나중에 백악관 집무실에서 기자들에게 "지난 며칠 동안 한국의 새 정부가 교회에 대한 습격을 벌였다는 소식을 들었다. 매우 악랄한 교회 습격이었다. 심지어 우리 군사 기지에도 들어가 정보를 얻어갔다"고 말했습니다.

“Some in Washington think the agreement benefits Korea too much, and different departments are surfacing calls to change it,” Lee told reporters aboard the presidential aircraft. “We can’t simply accept unilateral attempts to reopen what both presidents have already approved.”

Trump’s social media post highlighted a vulnerability that has haunted Lee in South Korea since he took office after a democratic election in June. His predecessor Yoon Suk Yeol’s decision to invoke martial law last December shocked the world, spooked markets and triggered the nation’s worst constitutional crisis in decades.

이 대통령은 대통령 전용기에서 기자들에게 "워싱턴의 일부 사람들은 이 협정이 한국에 너무 유리하다고 생각하며, 여러 부처에서 협정 변경을 요구하고 있다"고 말했습니다. "우리는 양국 대통령이 이미 승인한 것을 다시 협상하려는 일방적인 시도를 단순히 받아들일 수 없습니다."

트럼프 대통령의 소셜 미디어 게시물은 이 대통령이 6월 민주적 선거를 통해 취임한 이후 한국에서 그를 괴롭혀온 취약성을 부각시켰습니다. 그의 전임자인 윤석열 대통령이 지난 12월 계엄령을 선포한 결정은 세계를 충격에 빠뜨리고 시장을 불안하게 만들었으며, 수십 년 만에 최악의 헌법 위기를 촉발했습니다.

The US president quizzed his counterpart at the start of their meeting about the raids, but after Lee explained that the reports were an outgrowth of the political turmoil that predated the South Korean’s young presidency, Trump said, “I am sure it’s a misunderstanding.”

It was a sign that Lee’s efforts to charm Trump, honed in weeks of preparation for the meeting, had helped keep the talks on track.

미국 대통령은 회담 시작 시점에 이 대통령에게 습격에 대해 질문했지만, 이 대통령이 그 보도들이 젊은 이 대통령의 임기 이전에 일어난 정치적 격변의 결과라고 설명하자 트럼프 대통령은 "오해였을 거라고 확신한다"고 말했습니다.

이는 몇 주 동안의 회담 준비를 통해 갈고닦은 이 대통령의 트럼프 대통령을 매료시키려는 노력이 회담을 순조롭게 진행시키는 데 도움이 되었다는 신호였습니다.

상당히 잘 마무리된 편에 속하는 듯

Stocks Halt Rally as Yields Rise Before Price Data: Markets Wrap

https://www.bloomberg.com/news/articles/2025-08-24/asian-stocks-set-to-advance-after-powell-pivot-markets-wrap

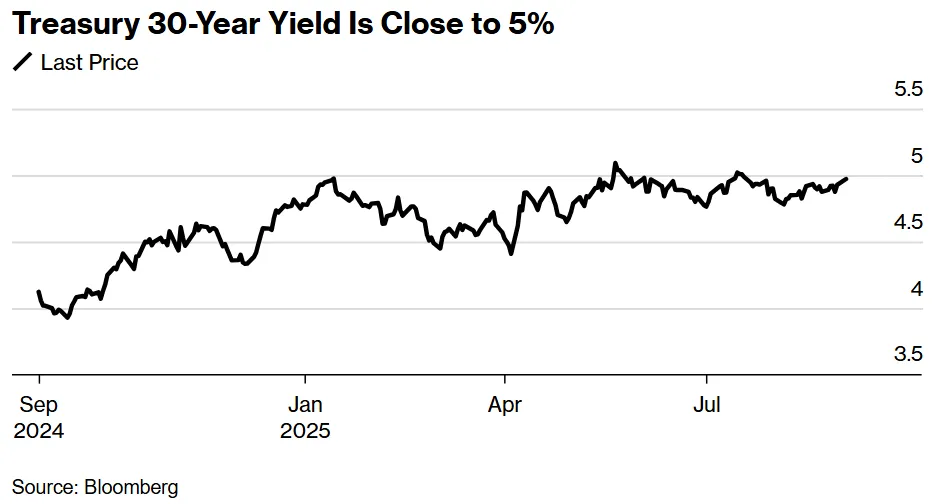

A rally that put stocks on the brink of all-time highs sputtered and bond yields rose as euphoria around Federal Reserve rate cuts eased just days ahead of a key inflation reading.

While Jerome Powell on Friday signaled a September rate cut is likely amid downside risks to the jobs market, doubts over the pace of those reductions lingered on Wall Street. In addition to officials remaining divided, traders are bracing for a not-so-friendly price reading later this week.

Policymakers are grappling with inflation that’s still above their 2% goal — and rising — and a labor market that’s showing signs of weakness. That unnerving reality, which pulls policy in opposite directions, is made worse by a high degree of uncertainty about how each of those factors will evolve over the coming months.

The Fed’s preferred gauge of underlying inflation probably ticked higher last month, with the personal consumption expenditures price index excluding food and energy rising 2.9% from a year ago. That would be fastest annual pace in five months.

금리 인하에 대한 연방준비제도(Fed)의 낙관론이 약해지면서 주가가 사상 최고치에 근접했던 랠리가 주춤하고 채권 수익률이 상승했습니다. 이는 주요 인플레이션 수치 발표를 불과 며칠 앞두고 나타난 현상입니다.

제롬 파월 의장은 금요일 고용 시장의 하방 위험이 있는 가운데 9월 금리 인하가 가능하다고 시사했지만, 월스트리트에서는 금리 인하 속도에 대한 의구심이 여전히 남아있습니다. 당국자들의 의견이 여전히 갈리는 데다, 투자자들은 이번 주 후반에 우호적이지 않은 물가 지수 발표에 대비하고 있습니다.

정책 입안자들은 여전히 목표치인 2%를 상회하며 상승하는 인플레이션과 약화 조짐을 보이는 노동 시장이라는 난관에 직면해 있습니다. 정책 방향을 상반되게 이끄는 이 불안정한 현실은 각 요인들이 앞으로 몇 달 동안 어떻게 변할지에 대한 높은 불확실성으로 인해 더욱 악화되고 있습니다.

연준이 선호하는 근원 인플레이션 지표는 지난달에 상승했을 가능성이 높으며, 식료품과 에너지를 제외한 개인소비지출(PCE) 물가지수는 전년 대비 2.9% 상승했습니다. 이는 5개월 만에 가장 빠른 연간 상승률이 될 것입니다.

Money markets are pricing in roughly 80% odds of a Fed rate cut in September, and a total of two reductions by the end of the year.

화폐 시장은 9월 연준의 금리 인하 가능성을 약 80%로, 연말까지 총 두 차례의 금리 인하를 예상하고 있습니다.

“If we are right, the focus shifts to what happens after September,” Guha said. “If the next set of labor data is not too bad, we think the Fed will begin to frame out the cautious recalibration cut, while seeking to contain expectations of ‘too much too soon’.”

구하(Guha)는 "우리의 예측이 맞다면, 초점은 9월 이후에 어떤 일이 일어날지로 옮겨갈 것"이라고 말했습니다. "만약 다음 고용 데이터가 그리 나쁘지 않다면, 연준은 '너무 성급하게 너무 많이'라는 기대를 억제하면서 조심스러운 재조정 인하를 시작할 것으로 생각한다"고 덧붙였습니다.

Dovish or hawkish cut?

“While we still see the Fed cutting in September, we now have to figure out whether it will be a ‘dovish cut’ or a ‘hawkish cut’,” said Andrew Brenner at NatAlliance Securities. “We don’t want one to think that inflation is not that important, but the real unknown risk to the economy is the employment situation.”

The exact path forward, particularly the pace of rate cuts, is still up for debate as Fed officials hold diverging views on the potential impact of tariffs and the overall state of the economy, according to Jason Pride and Michael Reynolds at Glenmede.

NatAlliance Securities의 앤드류 브레너는 "우리는 여전히 연준이 9월에 금리를 인하할 것으로 보고 있지만, 이제 '비둘기파적 인하'가 될지 '매파적 인하'가 될지 파악해야 한다"고 말했습니다. "인플레이션이 그리 중요하지 않다고 생각하고 싶지는 않지만, 경제에 대한 진정한 미지의 위험은 고용 상황이다"라고 덧붙였습니다.

Glenmede의 제이슨 프라이드와 마이클 레이놀즈에 따르면, 연준 관계자들이 관세의 잠재적 영향과 전반적인 경제 상황에 대해 서로 다른 견해를 가지고 있기 때문에, 정확한 향후 경로, 특히 금리 인하 속도는 여전히 논쟁의 여지가 있습니다.

Fed Bank of Dallas President Lorie Logan said money markets could face temporary pressures around quarter-end next month, though the US central bank still has room to continue reducing its balance sheet.

댈러스 연방준비은행 총재 로리 로건은 연준이 계속해서 대차대조표를 축소할 여지가 있지만, 다음 달 분기 말에 화폐 시장이 일시적인 압력에 직면할 수 있다고 말했습니다.

At Glenmede, the strategists noted that resuming the rate cut cycle will likely be a tailwind for bonds. Fixed income may offer upside potential for investors as yields across major fixed income categories remain near fair value.

“Small caps may stand to benefit most from easing, with more than half of their debt charging floating rate interest,” they said. “Lower interest expenses could notably lift earnings, potentially setting the stage for a small cap comeback into year-end.”

Glenmede의 전략가들은 금리 인하 사이클 재개가 채권에 순풍이 될 가능성이 높다고 언급했습니다. 주요 채권 범주의 수익률이 공정 가치 근처에 머물러 있어 채권은 투자자들에게 상승 잠재력을 제공할 수 있습니다.

그들은 "소형주는 부채의 절반 이상이 변동 금리로 되어 있어 금리 완화로 가장 큰 혜택을 볼 수 있다"고 말했습니다. "이자 비용이 낮아지면 수익이 크게 늘어나 연말까지 소형주가 반등할 수 있는 발판이 마련될 수 있다."

Aside from the macro picture, the next big test for the stock market will be a read on what’s been driving gains for the past few years: artificial-intelligence euphoria.

Nvidia Corp. - the last of the “Magnificent Seven” to report earnings - is due to unveil its results Wednesday after the close. Traders are hoping it can soothe fears about AI spending and effectively confirm that the stock market’s latest rally isn’t just a technology bubble.

거시적 상황 외에 주식 시장의 다음 큰 시험대는 지난 몇 년 동안 상승세를 이끌었던 인공지능(AI) 열풍에 대한 지표가 될 것입니다.

'매그니피센트 7' 중 마지막으로 실적을 발표하는 엔비디아는 수요일 장 마감 후 실적을 발표할 예정입니다. 투자자들은 엔비디아가 AI 지출에 대한 우려를 완화하고 최근 주식 시장 랠리가 단순한 기술 거품이 아님을 효과적으로 확신시켜주기를 바라고 있습니다.

“Those earnings will be good. The only question will be whether they’re good enough to push the stock higher after almost doubling over the past 4-5 months,” he added.

"그 실적은 좋을 것입니다. 유일한 의문은 지난 4~5개월 동안 거의 두 배로 오른 주가를 더 높일 만큼 충분히 좋을 것인가입니다."라고 그는 덧붙였습니다.

Nvidia’s size, it’s the biggest weight in the S&P 500 at almost 8%, and its position at the center of AI development have made it a bellwether of the broader market. The tech giant’s chips are everywhere, 40% of its revenue comes from Meta Platforms Inc., Microsoft Corp., Alphabet Inc. and Amazon.com Inc. — all are among the Top 10 weightings in the S&P 500.

Through several measures, big tech has become very influential, and that level of concentration suggests these stocks don’t just influence the market, but they increasingly drive the overall direction of travel, noted Anthony Saglimbene at Ameriprise.

엔비디아의 규모(S&P 500에서 거의 8%를 차지하는 가장 큰 비중)와 AI 개발의 중심에 있는 위치는 엔비디아를 전체 시장의 선행 지표로 만들었습니다. 이 기술 대기업의 칩은 어디에나 있으며, 매출의 40%는 메타 플랫폼스(Meta Platforms Inc.), 마이크로소프트(Microsoft Corp.), 알파벳(Alphabet Inc.), 아마존닷컴(Amazon.com Inc.)에서 나오는데, 이들 모두는 S&P 500에서 상위 10위권에 속하는 비중을 차지합니다.

Ameriprise의 앤서니 사글림벤은 여러 지표를 통해 볼 때 거대 기술 기업의 영향력이 매우 커졌으며, 이러한 집중도는 이들 주식이 시장에 영향을 미칠 뿐만 아니라 전체적인 방향을 점점 ...