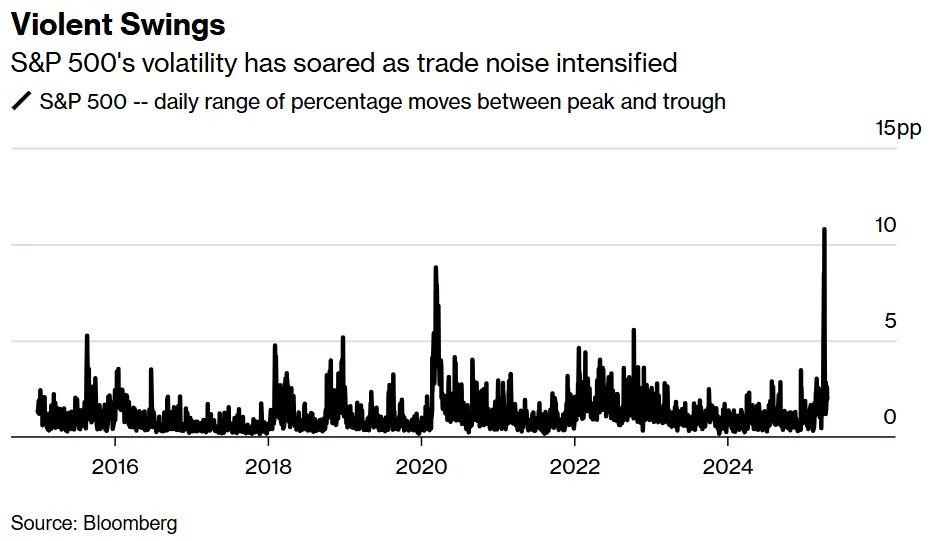

Global Money Managers Are Reluctant to Return to Chinese Stocks

Signs of a softening stance from the US on China tariffs may be a cue to buy the Asian nation’s stocks for some traders, but for long-term global funds the risk is still too high to pile into the market.

Money managers and strategists at Franklin Templeton, UBS Global Wealth Management and Jupiter Asset Management are among those expecting the trade war to be drawn out and inflict significant pain on the Chinese economy, making them cautious. Their wariness suggests any temporary detente will likely prove insufficient to lure back global funds en masse.

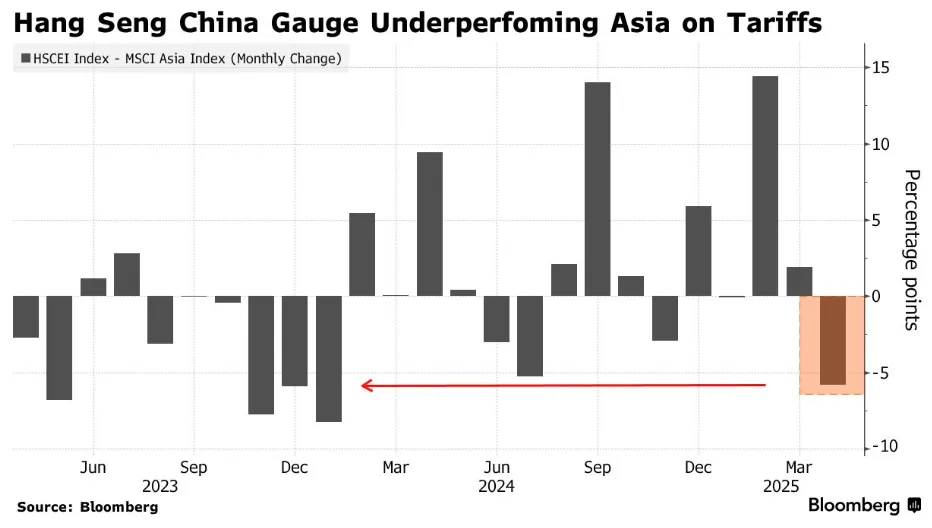

Although tariff optimism boosted an index tracking the biggest Chinese stocks listed in Hong Kong by more than 2% last week, it is still among the worst performers in Asia since the April 2 US tariff onslaught. The nation’s shares have missed out on inflows even as a rotation out of US assets benefited other markets such as Japan and Europe, according to Sanford C Bernstein.

“There are no signs of a sustainable inflow of funds into the China equity market,” said Hironori Akizawa, chief investment officer at Tokio Marine Asset Management International Pte. There will be a “tug of war” in the stock market as buying by those anticipating a trade deal will be countered by selling as investors examine the impact on the economy, he said.

미국이 중국 관세에 대해 누그러지는 태도를 보일 조짐은 일부 트레이더들에게는 아시아 국가 주식을 매수할 신호가 될 수 있지만, 장기 글로벌 펀드에게는 여전히 위험이 너무 커서 시장에 뛰어들기에는 어렵습니다.

프랭클린 템플턴, UBS 글로벌 자산 관리, 주피터 자산 관리의 자산 관리자 및 전략가들은 무역 전쟁이 장기화되고 중국 경제에 상당한 고통을 안겨줄 것으로 예상하는 이들 중 일부이며, 이로 인해 그들은 신중한 입장입니다. 그들의 경계심은 어떤 일시적인 데탕트(긴장 완화)도 글로벌 자금을 대거 유인하기에는 불충분할 것임을 시사합니다.

지난주 관세 낙관론이 홍콩에 상장된 중국 대형주를 추적하는 지수를 2% 이상 끌어올렸지만, 이 지수는 4월 2일 미국의 관세 공세 이후 아시아에서 여전히 최악의 성과를 내는 지수 중 하나입니다. 샌포드 C 번스타인에 따르면, 미국 자산에서 벗어나는 로테이션이 일본과 유럽 등 다른 시장에는 혜택을 주었음에도 불구하고 중국 주식은 자금 유입에서 소외되었습니다.

도쿄 해상 자산 관리 인터내셔널 Pte의 최고 투자 책임자 히로노리 아키자와는 "중국 주식 시장으로 지속 가능한 자금 유입의 조짐은 없다"고 말했습니다. 그는 무역 협상을 기대하는 매수세와 투자자들이 경제에 미치는 영향을 살피면서 발생하는 매도세로 인해 주식 시장에서 "줄다리기"가 벌어질 것이라고 말했습니다.

For China skeptics, its problems go beyond tariffs. Geopolitical tensions will be here to stay, and the ongoing economic decoupling with the US will disrupt industrial supply chains along the way. Apple Inc., for example, is seeking to build most iPhones that it sells in the US from India by the end of next year.

“It’s not just about tariffs, but more the real decoupling between these two economies which present risks for investors and for the Chinese economy,” said Sam Konrad, co-manager of the Jupiter Asian Income strategy.

중국 회의론자들에게 중국의 문제는 관세를 넘어섭니다. 지정학적 긴장은 계속될 것이며, 진행 중인 미국과의 경제적 디커플링(탈동조화)은 산업 공급망을 교란시킬 것입니다. 예를 들어, 애플은 내년 말까지 미국에서 판매하는 대부분의 아이폰을 인도에서 생산하려 하고 있습니다.

주피터 아시아 배당 전략의 공동 매니저인 샘 콘래드는 "단지 관세에 관한 것이 아니라, 투자자와 중국 경제에 위험을 초래하는 이 두 경제 간의 실질적인 디커플링에 더 가깝습니다"라고 말했습니다.

예… 저도 중국 주식을 직접 하긴 좀…

개인적으로 중국 주식은 풋옵션 매도 쳐놓은 거라고 생각…

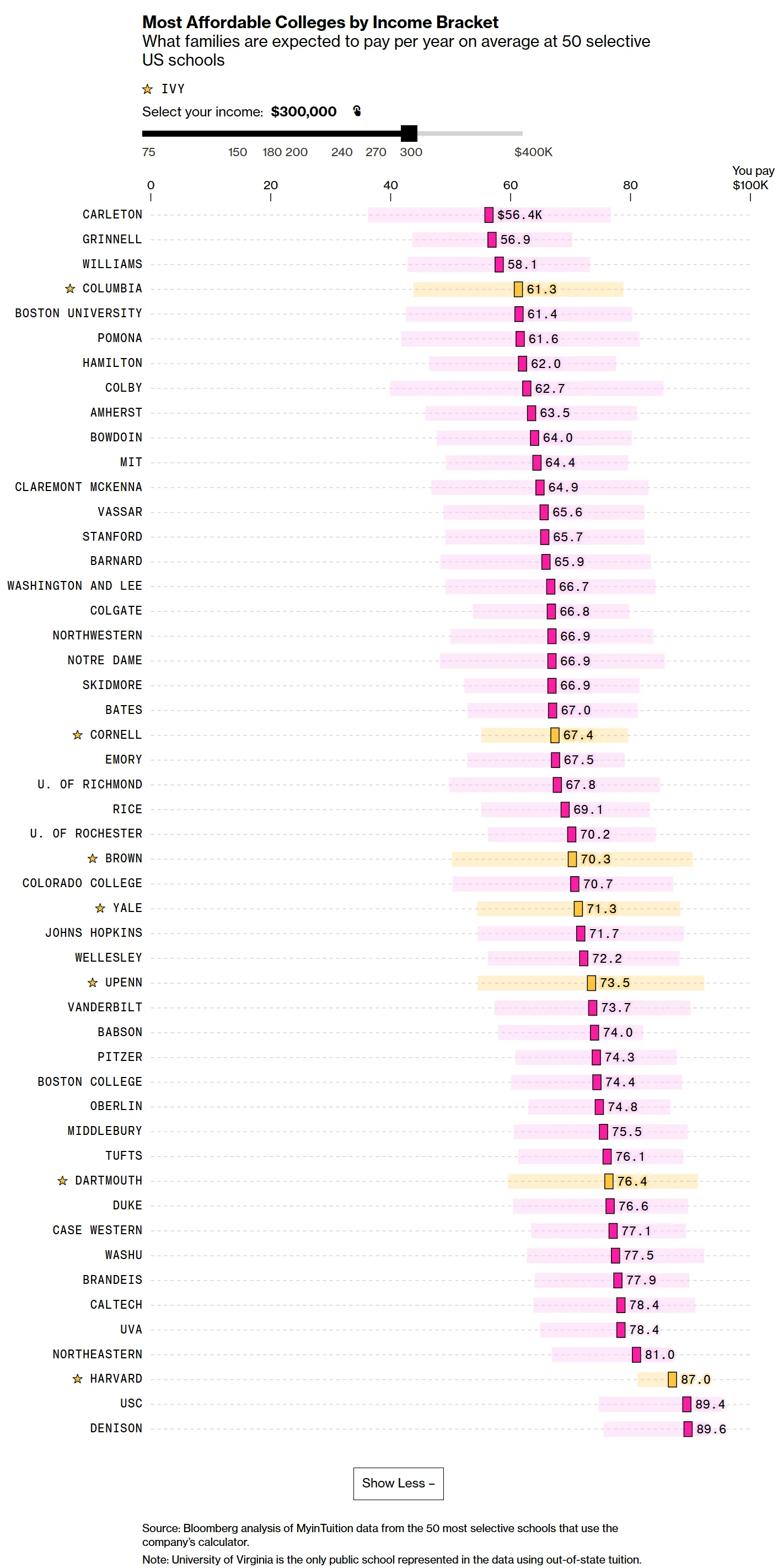

Top Colleges Are Too Costly Even for Parents Making $300,000

America’s middle class is getting squeezed by the soaring cost of attending elite colleges. And those schools — themselves pressured by attacks from the Trump administration over federal funding — are starting to get the message.

Harvard, MIT and the University of Pennsylvania have each in recent months expanded the range of students who qualify for free tuition to those from families earning up to $200,000. More Ivy League institutions and selective private colleges with robust endowments are expected to follow suit, as millions struggle to pay back student loans and schools grapple with growing backlash to how expensive it’s become to get a degree.

The new aid thresholds, which go into effect for the 2025-26 school year, are no coincidence. A Bloomberg analysis of financial aid data from 50 selective colleges shows that in many cases, middle-class families, defined by some metrics as making between $100,000 and $300,000, earn too much to qualify for meaningful aid but too little to afford college out of pocket.

미국의 중산층은 명문 대학 등록금 폭등으로 인해 어려움을 겪고 있습니다. 그리고 이들 학교들은 연방 자금에 대한 트럼프 행정부의 공격으로 인해 압박을 받으며 이러한 상황을 인지하기 시작했습니다.

하버드, MIT, 펜실베이니아 대학교는 최근 몇 달 동안 각각 연간 소득 20만 달러 이하 가구 학생들에게까지 무상 등록금 자격 범위를 확대했습니다. 수백만 명의 학생들이 학자금 대출 상환에 어려움을 겪고, 학교들은 학위 취득 비용이 얼마나 비싸졌는지에 대한 반발에 씨름하면서, 더 많은 아이비리그 대학과 튼튼한 기부금을 보유한 명문 사립 대학들도 이러한 움직임을 따를 것으로 예상됩니다.

2025-26학년도부터 적용되는 새로운 재정 지원 기준은 우연이 아닙니다. 50개 명문 대학의 재정 지원 데이터를 분석한 블룸버그의 분석에 따르면, 일부 기준에서 연 소득 10만 달러에서 30만 달러 사이로 정의되는 중산층 가구는 의미 있는 지원을 받기에는 너무 많이 벌고, 그렇다고 자비로 대학 등록금을 감당하기에는 너무 적게 버는 경우가 많습니다.

대들어서 당분간 정부 돈 못 받을 것 같으니까 이제야 미국에 계신 고객님들 생각이 난 미국 대학들

“The financial aid system ignores the reality of many people’s financial situation,” said Ayush Natarajan, 19, who was accepted in 2024 to his top choice: the $99,000-a-year University of Southern California. “They look at whether you’re low income or extremely wealthy, and leave out everyone in between.”

Natarajan, who lives in Los Angeles, was awarded around $5,500 in need-based aid from USC. That was a tough pill to swallow for his parents, who are helping his older brother pay for medical school and take home about $185,000 annually after federal and California income taxes. Natarajan opted to instead attend UCLA, where the in-state price tag is $42,000.

"재정 지원 시스템은 많은 사람들의 재정 상황 현실을 무시합니다"라고 서던 캘리포니아 대학교(USC)에 2024년 합격한 아유시 나타라잔(19세)이 말했습니다. USC는 연간 등록금이 9만 9천 달러로 그의 첫 번째 선택지였습니다. 그는 "그들은 당신이 저소득층인지 아니면 매우 부유한지 보고, 그 사이의 모든 사람을 놓칩니다"라고 덧붙였습니다.

로스앤젤레스에 사는 나타라잔은 USC로부터 필요 기반 지원금으로 약 5,500달러를 받았습니다. 연방세와 캘리포니아 주 소득세 후 연간 약 18만 5천 달러를 벌며 그의 형이 의과대학 학비를 내는 것을 돕고 있는 그의 부모님에게는 받아들이기 힘든 사실이었습니다. 나타라잔은 대신 주내 거주자 등록금이 4만 2천 달러인 UCLA에 다니기로 결정했습니다.

Sticker shock

Applying to college is a nerve-wracking process for families. Students stress over applications and whether they’ll get into top schools. And for parents, there’s the ever-escalating price tag, which is now nearly $100,000 a year at some universities. That makes higher education one of the largest expenses a family incurs. But there’s very little transparency when it comes to determining the actual costs, especially for families taking out loans.

That’s why many colleges have implemented “net price calculators” like MyinTuition, which was developed by Phillip Levine, an economics professor at Wellesley College. The tool offers estimates of what a family will have to pay based on a series of questions about a student’s financial profile, including income, home value and investment account balances. Once the student inputs their information the calculator offers a range of aid packages, listed as low, average and high.

Once students ...