Trump’s Interest Rate Obstacle Is Bigger Than Powell

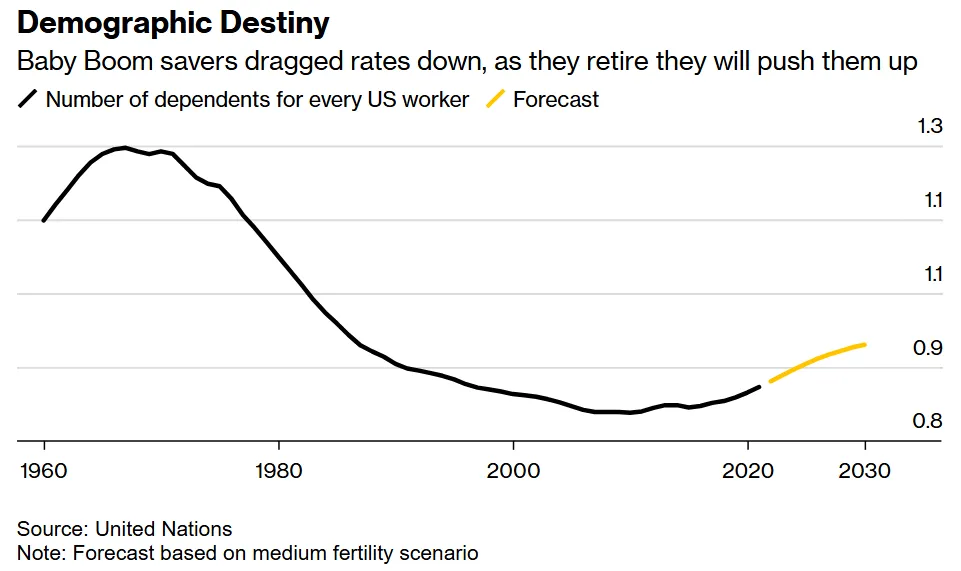

There are structural forces that drive the cost of borrowing, and right now they’re pointing up. Governments and businesses are piling on debt to pay for tax cuts, military spending, and AI investments — which means more demand for credit. As the Baby Boomers retire and China decouples from the US, the pool of saving to finance those loans is drying up.

Attacks on Fed independence risk shrinking the pool further. Investors don’t want to see the value of their hard-earned cash inflated away by a central bank under political control.

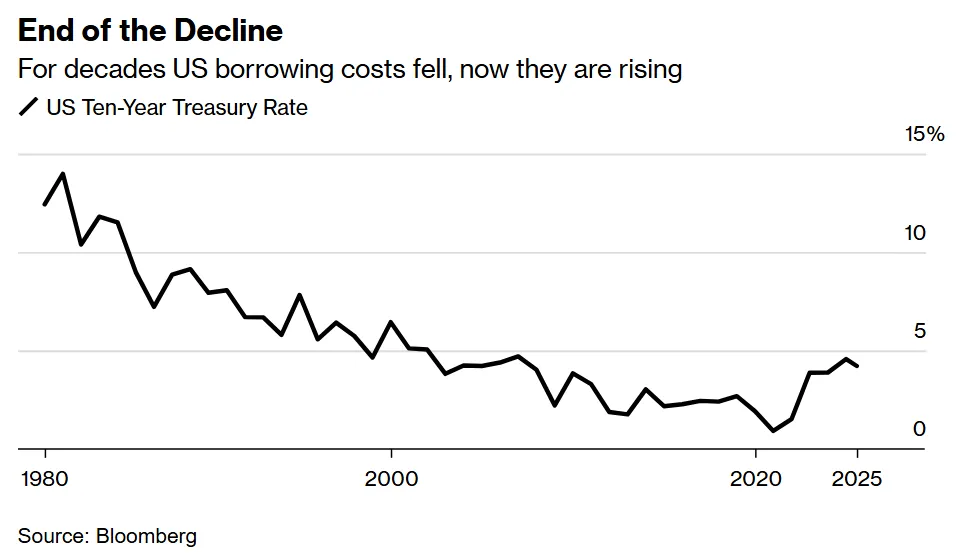

Add all of this together and it points to a world where 4.5% may be the new normal for ten-year Treasuries — the crucial rate for mortgages and corporate bonds, and the one Trump’s team says it wants to bring down. In fact, Bloomberg Economics analysis shows it’s more likely to trend above that figure than below it. For the world’s biggest economy, that means a wrenching transition.

For more than three decades, falling borrowing costs changed the whole landscape. Washington could rack up ever increasing debt without breaking the books. Cheap funds supercharged the US housing and stock markets. That’s all gone into reverse now, as the US faces a future where interest payments cost more than defense spending, and 7% mortgage rates bite into home prices.

정부와 기업들이 감세, 국방비, 인공지능(AI) 투자에 필요한 자금을 마련하기 위해 부채를 늘리면서 신용 수요가 증가하고 있습니다. 한편, 베이비붐 세대의 은퇴와 중국과 미국의 탈동조화로 인해 대출 자금으로 활용될 저축 규모는 줄어들고 있습니다.

여기에 연방준비제도(Fed)의 독립성 훼손 가능성까지 더해지면 저축 규모는 더 줄어들 위험이 있습니다. 투자자들은 정치적 통제 하에 있는 중앙은행으로 인해 자신이 힘들게 모은 돈의 가치가 인플레이션으로 사라지는 것을 원치 않기 때문입니다.

이러한 요인들을 종합해 보면 10년 만기 미국 국채 금리(모기지와 회사채의 기준이 되는 중요한 금리)가 4.5%를 새로운 기준으로 삼게 될 가능성이 높습니다. 이는 트럼프 팀이 낮추고 싶어하는 수치이기도 합니다. 블룸버그 이코노믹스 분석에 따르면 10년 만기 국채 금리가 4.5%보다 낮아지기보다는 그 이상으로 오를 가능성이 더 높습니다. 세계 최대 경제 대국인 미국에게는 힘든 전환기가 될 것입니다.

지난 30년 이상 금리 하락은 모든 것을 바꿔놓았습니다. 워싱턴은 장부를 망가뜨리지 않고도 계속해서 부채를 늘릴 수 있었습니다. 저금리는 미국 주택 시장과 증시를 활성화했습니다. 하지만 이제 모든 것이 역전되었습니다. 미국은 이제 국방비보다 이자 비용이 더 많이 들고, 7%대의 모기지 금리가 주택 가격에 부담을 주는 미래에 직면했습니다.

All this is a corrective to Trump’s claim that a new Fed chief can fix everything. True, Powell controls short-term borrowing costs, and in the months ahead the chances are he’ll be guiding them lower. Signs of weakness in the labor market and the early exit of Fed Governor Adriana Kugler — which means an opportunity for Trump to appoint a low-rates loyalist to replace her — both raise the odds of a September rate cut.

Looking through the ups and downs of the cycle, though, there’s a deeper logic at work. The price of money — like any other price — is set by the balance of supply and demand. More supply of savings means rates fall. More investment demand means they rise.

In the economics textbooks, the price of money that balances supply of saving and demand for investment, whilst keeping employment high and inflation low, has a name: the natural rate of interest. For more than three decades from the early 1980s to the mid-2010s, it was falling. Now, it’s rising.

What drove the decline? Lots of things.

On the saving side, the Baby Boom generation — born in the years immediately after World War II — were working hard and stashing away funds for retirement. China was running a massive trade surplus, and — to prevent its currency appreciating — recycling export earnings into Treasuries. Saudi Arabia and the other petrostates were in a similar position — with income from oil exports parked in US government debt.

이 모든 상황은 새로운 연준 의장이 모든 것을 해결할 수 있다는 트럼프의 주장에 대한 반론을 제시합니다. 물론 파월 의장은 단기 금리를 통제하며, 앞으로 몇 달 동안은 금리를 낮출 가능성이 높습니다. 노동 시장의 약화 징후와 연준 이사 아드리아나 쿠글러의 조기 사임(트럼프가 낮은 금리를 지지하는 충성파를 후임으로 임명할 기회)은 9월 금리 인하 가능성을 높입니다.

하지만 경기 순환의 오르내림을 넘어 더 깊은 논리가 작용하고 있습니다. 돈의 가격은 다른 모든 가격과 마찬가지로 수요와 공급의 균형에 의해 결정됩니다. 저축의 공급이 많으면 금리는 하락하고, 투자 수요가 많으면 금리는 상승합니다.

경제 교과서에서 저축의 공급과 투자의 수요의 균형을 맞추고 고용을 높게 유지하며 인플레이션을 낮게 유지하는 돈의 가격을 자연 이자율이라고 부릅니다. 1980년대 초부터 2010년대 중반까지 30년 넘게 자연 이자율은 하락했습니다. 하지만 이제는 상승하고 있습니다.

하락의 원인은 다양합니다.

저축 측면에서는 제2차 세계대전 직후에 태어난 베이비붐 세대가 열심히 일하고 은퇴를 위해 자금을 저축했습니다. 중국은 막대한 무역 흑자를 기록했고, 위안화 가치 상승을 막기 위해 수출 수익을 미국 국채에 재투자했습니다. 사우디아라비아를 비롯한 산유국들도 비슷한 상황이었는데, 석유 수출로 얻은 수입을 미국 정부 부채에 맡겼습니다.

Fed independence — with presidents from Ronald Reagan to Barack Obama staying out of interest rate decisions — provided assurance that the value of savings wouldn’t be inflated away, reinforcing the safe haven appeal of Treasury debt.

On the investment side, the golden years of rapid productivity gains that followed World War II were fading into memory. As US growth fell from an average above 4% in the 1960s to below 2% in the 2000s, opportunities for profitable investment fell with it. The end of the Cold War meant a peace dividend, with lower defense spending helping to keep government borrowing under control. In 2001, the US debt was just above 30% of GDP, and the government ran a budget surplus.

로널드 레이건부터 버락 오바마에 이르기까지 역대 대통령들이 금리 결정에 관여하지 않고 연준의 독립성을 보장하면서 저축 가치가 인플레이션으로 사라지지 않을 것이라는 확신을 주었고, 이는 미국 국채의 안전 자산으로서의 매력을 강화했습니다.

투자 측면에서는 제2차 세계대전 이후의 황금기였던 빠른 생산성 향상은 추억 속에 흐려졌습니다. 1960년대 평균 4% 이상이었던 미국의 성장률이 2000년대 2% 아래로 떨어지면서 수익성 있는 투자 기회도 함께 줄었습니다. 냉전 종식으로 인한 '평화 배당금'으로 국방비 지출이 줄어들어 정부 부채를 억제하는 데 도움이 되었습니다. 2001년 미국의 부채는 GDP의 30%를 조금 넘는 수준이었고, 정부는 예산 흑자를 기록했습니다.

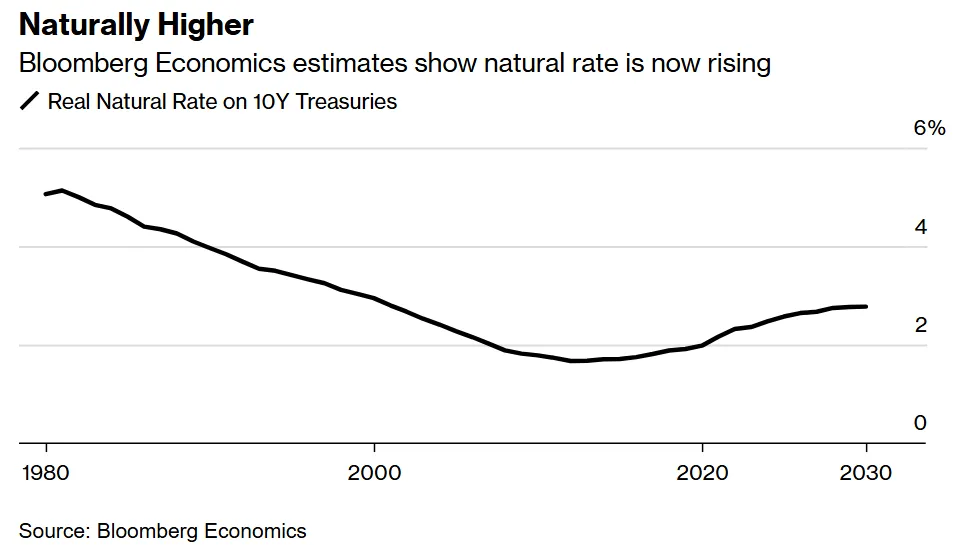

Putting those pieces together, abundant supply of savings and scant demand for investment meant the natural rate on long-term borrowing fell. Bloomberg Economics calculations show a drop from an inflation-adjusted high of about 5% in the early 1980s to a low of about 1.7% in 2012.

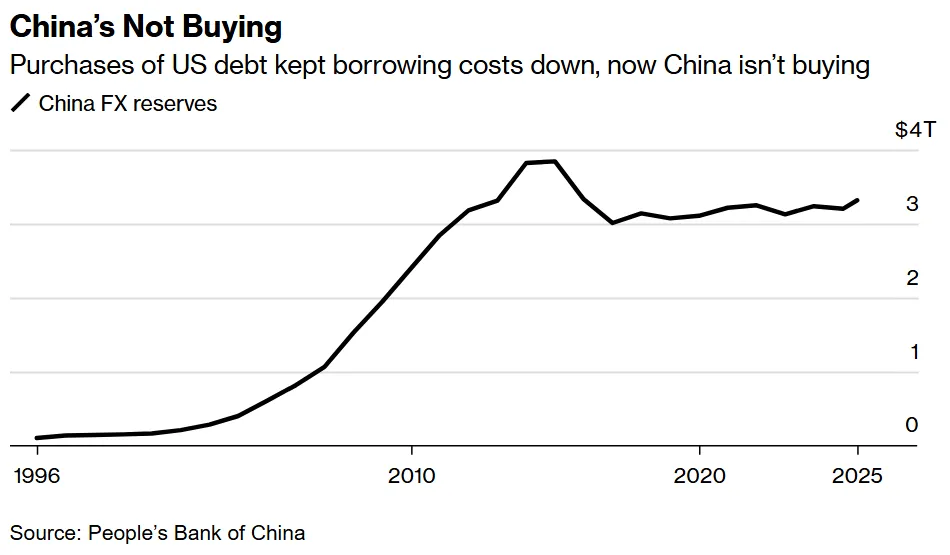

Now, those trends are swinging into reverse. The Baby Boom generation are retiring — spending their pensions, rather than adding savings to the pot. China has let its currency float — which means no more need to buy dollars to prevent it appreciating. From the early 1990s to 2014, China’s FX reserves rose from near zero to almost $4 trillion. Since then, they have dropped to $3.3 trillion.

풍부한 저축 공급과 적은 투자 수요가 장기 대출의 자연 이자율을 낮췄습니다. 블룸버그 이코노믹스 계산에 따르면, 물가상승률을 감안한 실질 금리는 1980년대 초 약 5%의 최고치에서 2012년 약 1.7%의 최저치까지 떨어졌습니다.

하지만 이제 이러한 추세는 역전되고 있습니다. 베이비붐 세대는 은퇴하면서 저축을 늘리기보다는 연금을 소비하고 있습니다. 중국은 자국 통화인 위안화를 변동 환율제로 전환하여 위안화 가치 상승을 막기 위해 달러를 매입할 필요가 없어졌습니다. 1990년대 초부터 2014년까지 중국의 외환 보유고는 거의 0에서 약 4조 달러까지 증가했지만, 그 이후 3조 3천억 달러로 감소했습니다.

Saudi Arabia and the other petrostates have followed a similar trajectory — pivoting from Treasury purchases to higher spending on projects closer to home and bets on the businesses of tomorrow. Investment in Neom — Crown Prince Mohammed bin Salman’s futuristic city in the desert — may run into trillions of dollars.

Geopolitics also plays a role. In 2022, following Russia’s invasion of Ukraine, the US and its allies froze about $300 billion in Kremlin assets. The target — cutting off funds for Putin’s war machine. The collateral damage — turning Treasury debt into a tool of economic statecraft, and so reducing its value as a reserve asset. Other countries don’t want to put their savings in the US if the US can seize their savings.

A more dangerous world has ended the peace dividend, forcing governments to increase defense spending. Europe’s NATO members have agreed to raise their military budgets to 3.5% of GDP, up from an earlier target of 2%. Bloomberg Economics calculates that borrowing to pay for that increase would add about $2.3 trillion to Europe’s debt over the next decade.

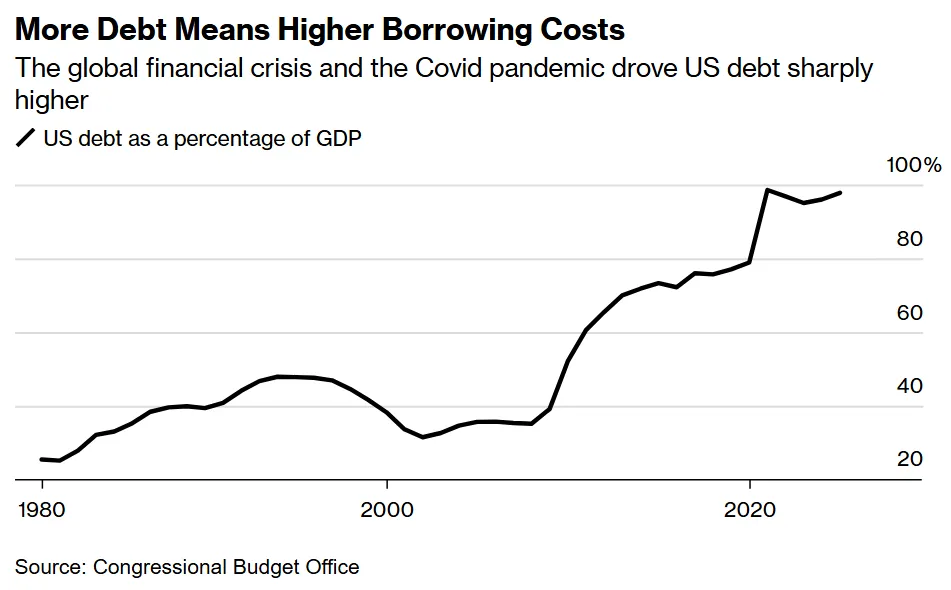

With investors treating German and French debt as a close substitute for that of the US, more borrowing in Berlin and Paris means higher rates for Washington. US debt approaching 100% of GDP adds to the strain.

The retirement of the baby boomers, the end of the savings glut from China and the petrostates, and more borrowing from governments have changed the arrow on the natural rate from down to up. Bloomberg Economics calculations suggest it has already climbed from a nadir of 1.7% in 2012 to around 2.5% in 2024. Based on plausible trajectories for demographics, debt and other factors, it will climb to 2.8% by 2030 — keeping the ten-year Treasury rate lodged between 4.5% and 5%.

사우디아라비아와 다른 산유국들도 비슷한 궤적을 보이고 있습니다. 국채 매입에서 벗어나 자국 내 프로젝트와 미래 사업에 대한 투자에 더 많은 지출을 하고 있습니다. 무함마드 빈 살만 왕세자의 사막의 미래 도시인 네옴 프로젝트에 대한 투자는 수조 달러에 달할 수 있습니다.

지정학적 요인도 한몫하고 있습니다. 2022년 러시아의 우크라이나 침공 이후, 미국과 동맹국들은 러시아 정부 자산 약 3천억 달러를 동결했습니다. 이는 푸틴의 전쟁 자금을 차단하기 위한 조치였습니다. 하지만 부수적인 피해로 인해 국채가 경제적 국가 통치의 도구로 변질되었고, 결과적으로 국채의 준비 자산으로서의 가치가 하락했습니다. 다른 나라들은 미국이 언제든 자신들의 저축을 압류할 수 있다면 미국에 저축을 하고 싶지 않을 것입니다.

더 위험해진 세계는 평화 배당금을 끝냈고, 정부들은 국방비를 늘릴 수밖에 없게 되었습니다. 유럽의 나토 회원국들은 국방 예산 목표를 기존 GDP의 2%에서 3.5%로 올리기로 합의했습니다. 블룸버그 이코노믹스는 이로 인해 유럽의 부채가 향후 10년간 약 2조 3천억 달러 증가할 것으로 추산했습니다.

투자자들이 독일과 프랑스 국채를 미국 국채의 대체재로 여기면서, 독일과 프랑스의 차입이 늘어나면 미국의 금리도 높아집니다. 미국의 부채가 GDP의 100%에 육박하는 것도 부담을 가중시키고 있습니다.

베이비붐 세대의 은퇴, 중국과 산유국의 저축 과잉 종료, 정부 차입 증가로 인해 자연 이자율의 화살표는 하락에서 상승으로 바뀌었습니다. 블룸버그 이코노믹스 계산에 따르면, 자연 이자율은 2012년 최저치인 1.7%에서 2024년 현재 약 2.5%까지 올랐습니다. 인구 통계, 부채 등 기타 요인들의 그럴듯한 궤적을 바탕으로 볼 때, 2030년에는 2.8%까지 상승하여 10년 만기 국채 금리가 4.5%에서 5% 사이에 머무르게 될 것입니다.

That might seem like a small increase. For a move in the base rate that determines the price of money across the whole global financial system, it’s seismic. And risks are tilted toward higher, not lower.

이는 작은 상승처럼 보일 수 있습니다. 하지만 전 세계 금융 시스템의 돈 가격을 결정하는 기준 금리의 변화는 엄청난 것입니다. 게다가 이러한 위험은 낮아지기보다는 높아지는 쪽으로 기울어져 있습니다.

If Trump does appoint a low-rates loyalist as the next Fed chair, he will get a lower short-term policy rate. By eroding the Fed’s credibility as an inflation fighter, though, he would risk driving long-term borrowing costs higher as global savings flow out of US markets.

If all of those forces collide, the impact could be even higher borrowing costs — with the natural rate above 4% and the ten-year Treasury at a nose-bleed inducing 6% or higher.

Some caveats are in order. The natural rate is as tough to track down as it is central to the operation of the economy and financial system. The error band around estimates of where it was in the past or is today are wide. The error band around where it is headed in the future is wider.

Not everything about the low rates world we’re leaving behind was good, and not everything about the higher rates world to come is bad. Indeed, the slow growth and dearth of investment opportunities of the 2010s was nothing to celebrate. If borrowing costs are higher because AI is driving opportunities for rising prosperity and the world is getting serious about fighting climate change, that would be a positive.

Still, something important has changed. For more than three decades, borrowing costs in the US — and around the world — were falling. Now, they’re rising. For everyone from the US Treasury, to the hedge fund titans of Wall Street, to 401(k) investors, that’s a wrenching transition. For Trump, it’s not one that firing Powell will do anything to change.

만약 트럼프가 차기 연준 의장으로 저금리를 선호하는 인사를 임명한다면, 단기 정책 금리는 낮아질 것입니다. 하지만 이는 연준이 인플레이션 파이터로서의 신뢰도를 훼손하여 글로벌 저축 자금이 미국 시장에서 빠져나가게 만들고, 결과적으로 장기 차입 비용을 더 높일 위험이 있습니다.

이러한 모든 요인들이 충돌하면, 그 영향으로 차입 비용은 훨씬 더 높아질 수 있습니다. 자연 이자율이 4%를 넘고 10년 만기 국채 금리가 6% 이상으로 치솟을 수도 있습니다.

물론 몇 가지 주의할 점이 있습니다. 자연 이자율은 경제와 금융 시스템의 작동에 매우 중요하지만, 파악하기가 매우 어렵습니다. 과거와 현재의 자연 이자율 추정치에는 오차 범위가 넓고, 미래에 대한 예측은 그보다 훨씬 더 넓습니다.

우리가 떠나고 있는 저금리 시대의 모든 것이 좋았던 것은 아니며, 다가올 고금리 시대의 모든 것이 나쁜 것도 아닙니다. 실제로 2010년대의 낮은 성장률과 투자 기회 부족은 결코 축하할 일이 아니었습니다. 만약 인공지능(AI)이 번영을 위한 기회를 창출하고 전 세계가 기후 변화에 진지하게 맞서 싸우면서 차입 비용이 높아진다면, 이는 긍정적인 신호일 수 있습니다.

그럼에도 불구하고 중요한 변화가 일어났습니다. 30년 넘게 미국과 전 세계의 차입 비용은 하락했습니다. 하지만 이제는 상승하고 있습니다. 미국 재무부부터 월스트리트의 헤지펀드 거물, 401(k) 투자자에 이르기까지 모두에게 이것은 힘든 전환기입니다. 트럼프가 파월을 해고한다고 해도 이 흐름은 바뀌지 않을 것입니다.

OPEC+ Leaves Traders With Cliffhanger as Stormy Chapter Ends

OPEC+ closed a two-year chapter in its oil strategy on Sunday with the last in a series of bumper oil production increases. But it left crude traders with a cliffhanger.

Saudi Arabia and its partners have stunned oil markets and capped futures prices in recent months by pushing more barrels into a fragile global market, offering relief to consumers and a fillip for President Donald Trump.

The 547,000 barrel-a-day output increase they approved on Sunday completes the reversal — one year ahead of schedule — of a giant supply cutback made in 2023. The Organization of the Petroleum Exporting Countries and its allies have fast-tracked the revival in a bid to reclaim market share.

Yet they also have unfinished business: another layer of supplies, also halted two years ago, amounting to 1.66 million barrels a day, which is currently due to remain offline until late 2026. And on Sunday delegates were offering less, rather than more, clarity regarding its fate.

Depending on oil market conditions, the coalition could press on with restarting this tranche, officials said. Or, as some delegates suggested last month, the producers could take a pause. Alternatively, if markets slump, they might even completely reverse the recent surge. A follow-up meeting was set for Sept. 7 to review the situation.

“The messaging coming from today’s voluntary producer meeting is that all options remain on the table — including bringing those barrels back, pausing increases for now, or even reversing the recent policy action,” said Helima Croft, head of commodity strategy at RBC Capital Markets LLC.

Based on the outlook for the months ahead, OPEC+ may...