수익없는 위험을 쫓지 말라. Return Free Risk - Terry Smith

Reaching

2025.07.12조회수 69회

Reaching

구독자 102명구독중 44명

모든 것이 완벽한 여행이었다.

매일 웃으며 사랑하며 건강하게 살고 있습니다.

73권 독서 기록 / 1500권 목표,

요가수련 14개월차, 디지털 노마드, 세계 여행이 목표.

출처: https://www.fundsmith.co.uk/media/hafpybqk/return-free-risk-pdf.pdf

Efficient markets? The efficient-market hypothesis (EMH) asserts that financial markets are “efficient” in that an investor cannot consistently achieve returns in excess of average market returns on a risk-adjusted basis. Thus we are taught that achieving higher return is only possible with the assumption of higher risk. Whilst this may strike a chord with investors’ instincts that there is no such thing as a free lunch, there is a large and growing body of evidence that whilst it may fit with the EMH and investors' gut instincts, it is not necessarily true in practice.

효율적 시장? 효율적 시장 가설(EMH)은 금융시장이 ‘효율적’이며, 투자자는 위험을 감안한 기준에서 평균 시장 수익률을 초과하는 수익을 지속적으로 얻을 수 없다고 주장한다. 따라서 우리는 더 높은 수익을 얻으려면 더 높은 위험을 감수해야 한다는 것을 배우게 된다. 이는 ‘공짜 점심은 없다’는 투자자의 본능적인 직관과 일치할 수 있지만, EMH와 투자자들의 직감에 부합한다고 해도 실제 현실에서는 반드시 진실이라고 할 수 없다는 방대한 양의 증거들이 존재하며, 그 수는 계속해서 증가하고 있다.

Less volatile stocks produce higher returns. Research by Robert Haugen of Haugen Financial Systems and Nardin Baker, chief strategist at Guggenheim Partners (source: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2055431), shows that between 1990 and 2011 in 21 developed countries, the least volatile decile of stocks generated annualised total returns of 8.7% while the most volatile decile lost 8.8% pa. In US equities, the least volatile decile made average returns of 12% pa over the same period whilst the most volatile lost 7% pa. 12 emerging markets covered by the study for the period 2001–2011 produced similar results.

변동성이 적은 주식이 더 높은 수익을 낸다. Haugen Financial Systems의 로버트 하우겐과 Guggenheim Partners의 수석 전략가 나딘 베이커의 연구에 따르면(출처: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2055431), 1990년부터 2011년까지 21개 선진국에서 변동성이 가장 낮은 상위 10% 주식은 연평균 총수익률 8.7%를 기록한 반면, 변동성이 가장 높은 하위 10% 주식은 연평균 –8.8%의 손실을 기록했다. 미국 주식시장에서도 같은 기간 동안 변동성이 가장 낮은 10% 주식은 연평균 12%의 수익을 올렸지만, 가장 변동성이 높은 주식군은 연평균 =7% 손실을 입었다. 2001년부터 2011년까지 12개 신흥국 시장에서도 이와 유사한 결과가 나타났다.

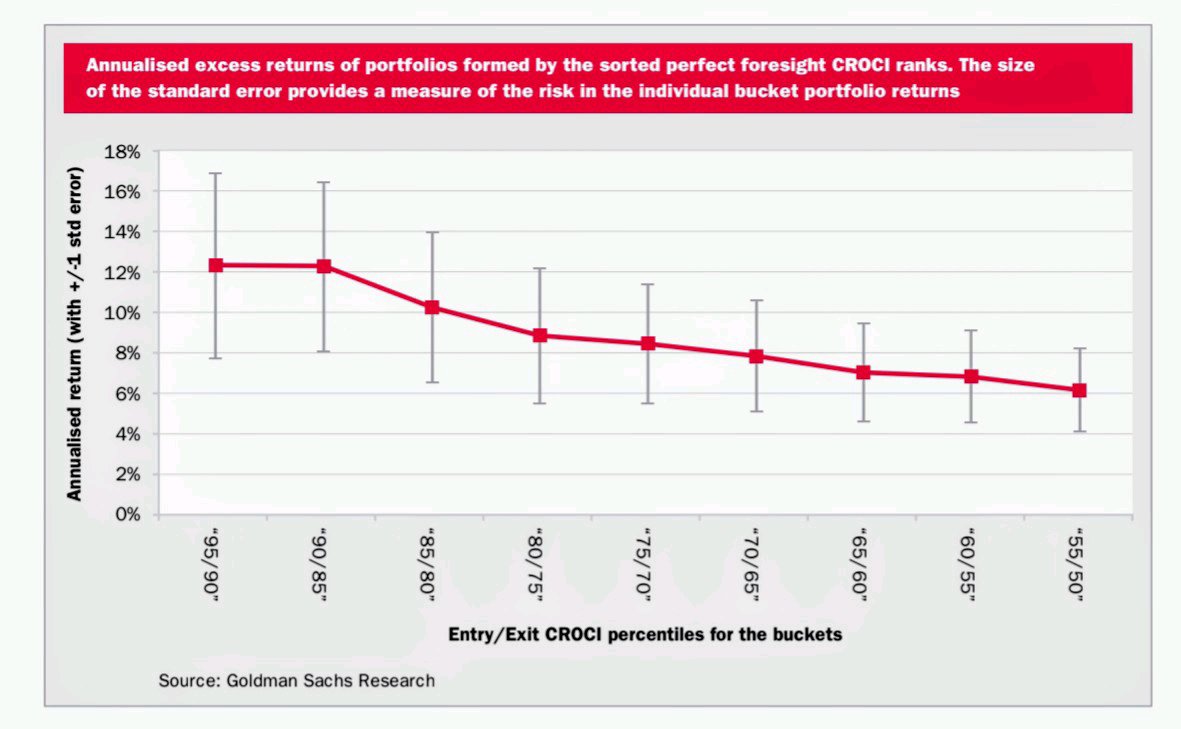

Annualised excess returns of portfolios formed by the sorted perfect foresight CROCI ranks. The size of the standard error provides a measure of the risk in the individual bucket portfolio returns.

완벽한 선견지명을 가진 CROCI 순위에 따라 정렬된 포트폴리오들에서의 연환산 초과 수익률. 각 개별 버킷 포트폴리오 수익률에 대한 위험 ...

ㄷ ㄷ ㄷ

딩동댕

![[책] 세계 경제 지각 변동 요약 -박종훈 저 [완]](https://post-image.valley.town/slq5i7-YbaUZjpWN1fcH9.png)

![[책] 퀄리티 투자, 그 증명의 기록 - 테리 스미스 [1]](https://post-image.valley.town/5y83KkuAzV-M8Ys6xntB4.png)

![[책] 거인의 어깨 1 요약 - 홍진채 저 [1]](https://post-image.valley.town/0OzIFVqD9LZLA_8YnV4Y1.png)