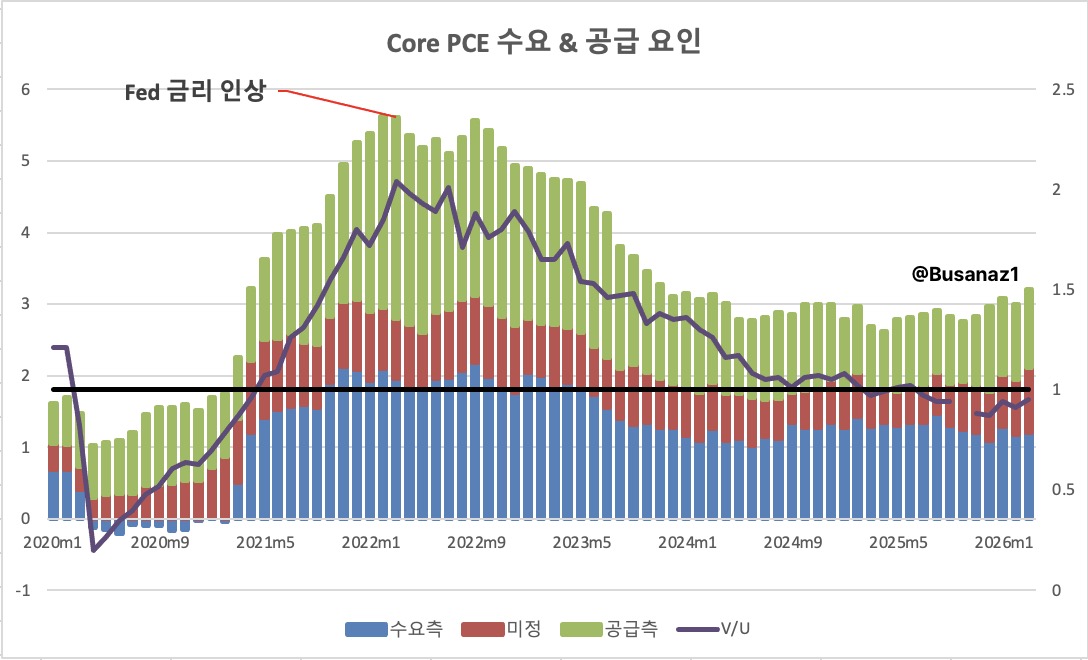

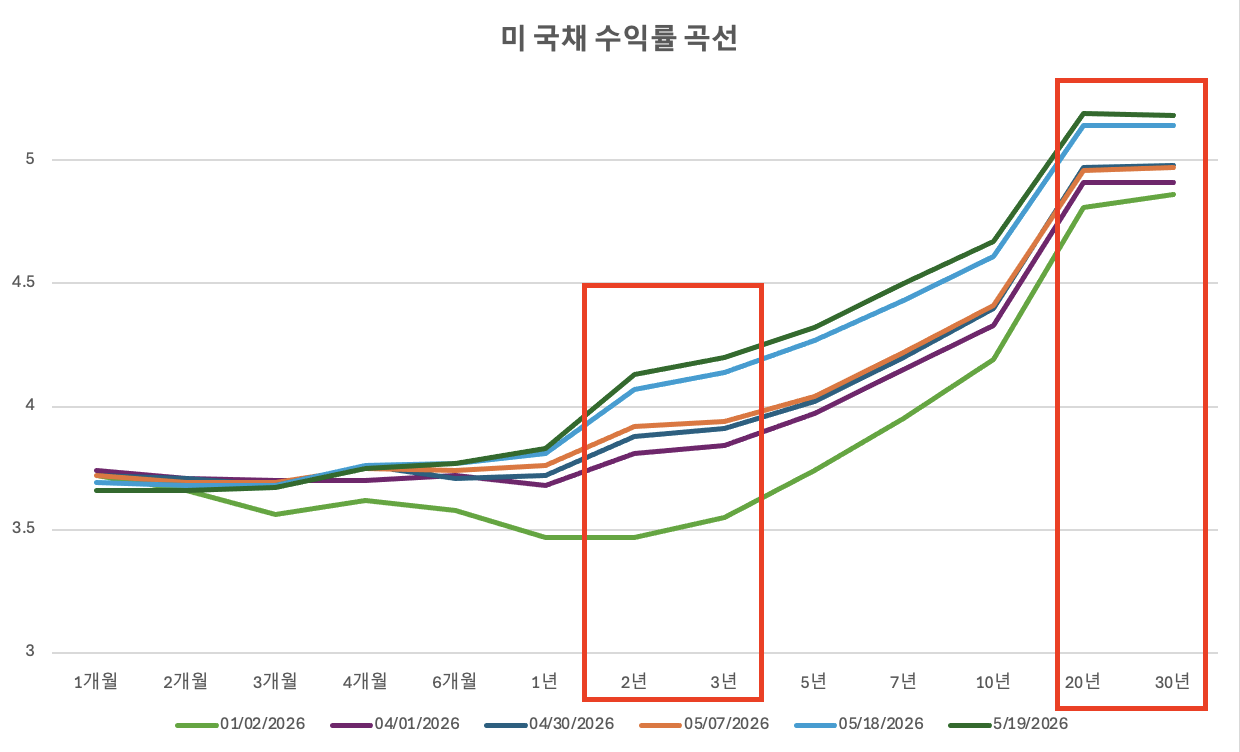

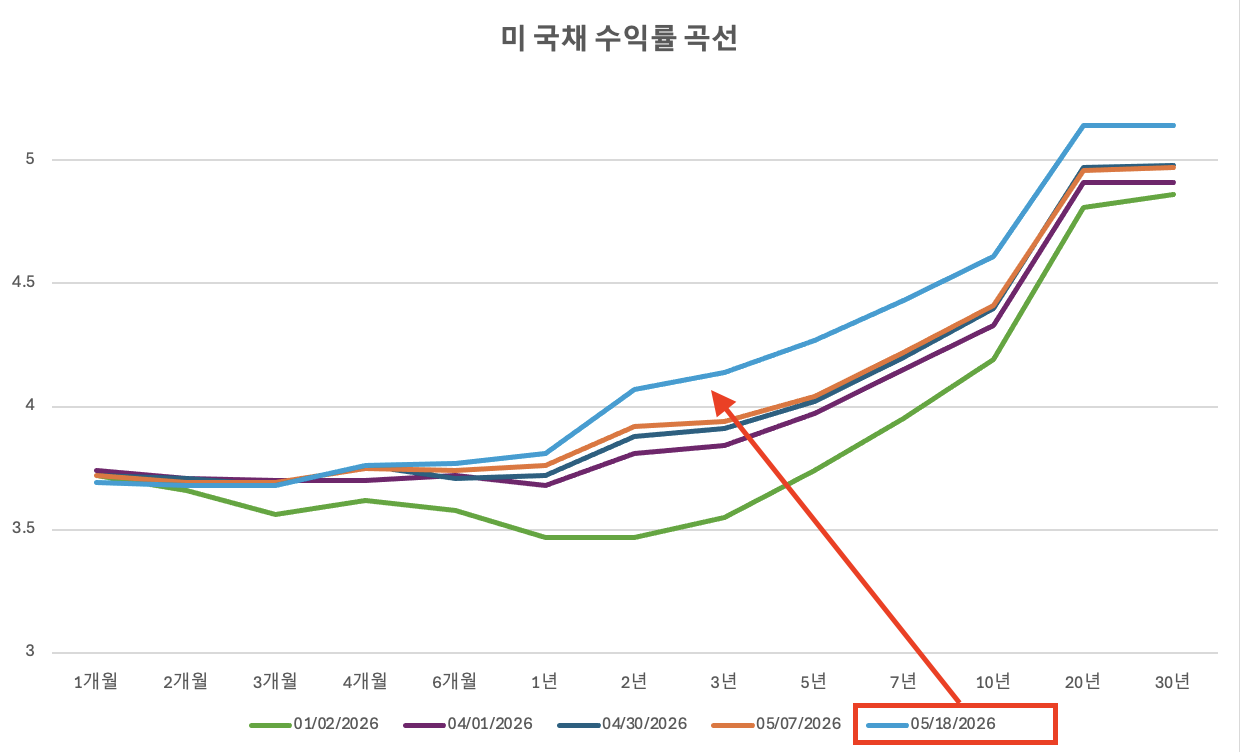

기대인플레에 대한 좋은 교육 자료^^ - 크리스토퍼 월러 이사 발언 중 (핵심 : Bayesian Updating)

Busanaz1

2026.05.27조회수 100회

Busanaz1

구독자 413명구독중 14명

개인적인 시각으로 경제 이야기를 합니다.

With regard to this last statement, there is a theoretical puzzle that I have been thinking about. If people know that each shock in a sequence of price shocks is transitory, then why might they expect average inflation to increase in the future when observing this sequence of shocks? Let me give a simple example. If you flipped a coin and won a dollar each time it came up heads and lost a dollar every time it came up tails, your expected winnings from the next flip of the coin would be zero. This would still be true even if the last three coin flips came up heads. But when forming this expectation, it is assumed that the flips are independent and uncorrelated. And we all make this assumption when calculating this expectation. Expectations formed this way are based on classical probability theory—in this ...

역시 괜히 연준 이사로 활동하는 게 아니네요...

소로스의 재귀성과 유사한 느낌인 것 같습니다.

좋은 글 감사해요!